In the evolving landscape of decentralized finance, the ability to borrow USDC against TradFi credit score on-chain marks a pivotal shift from overcollateralized models to undercollateralized lending powered by real-world financial data. Platforms like 3Jane are pioneering this frontier, enabling users to access USDC credit lines without locking up crypto assets, simply by leveraging verifiable traditional credit assessments alongside on-chain activity. This approach not only democratizes access to liquidity but also integrates the predictability of TradFi risk models with the efficiency of smart contracts.

Mechanics of On-Chain Undercollateralized Loans

Traditional DeFi lending protocols demand borrowers deposit assets worth 150-200% of the loan value to mitigate liquidation risks, a barrier that excludes many users with illiquid holdings. In contrast, on-chain undercollateralized loans via 3Jane employ algorithmic underwriting that pulls from off-chain sources like bank balances and credit bureau data, processed through privacy-preserving oracles. The protocol's credit graph aggregates these signals into a dynamic score, determining eligibility for unsecured USDC disbursements. Lenders deposit USDC to mint protocol-native assets like USD3, earning yields while borrowers repay via automated schedules enforced on Ethereum.

This model reduces capital inefficiency; where Aave or Compound might require $150,000 collateral for a $100,000 loan, 3Jane assesses holistic creditworthiness to approve similar amounts collateral-free. Early data suggests interest rates calibrated from 5-27% based on risk profiles, blending peer-to-pool dynamics with real-time adjustments.

Key Prerequisites for Crypto Borrowing No Collateral

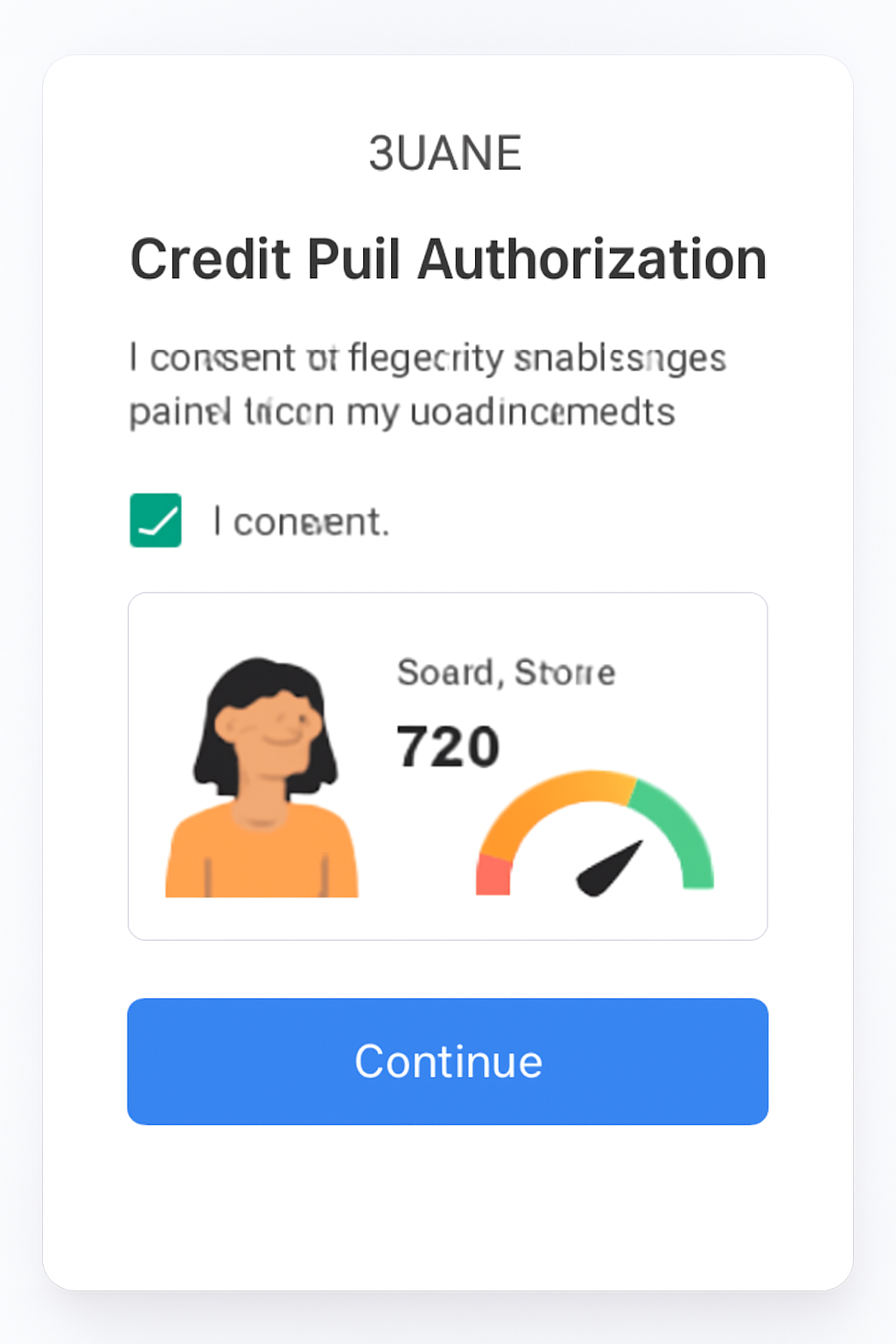

Before diving into the protocol, verify your setup aligns with 3Jane's requirements. A robust Ethereum wallet such as MetaMask ensures seamless interaction, while linking via Plaid unlocks bank data without exposing credentials. Credit scores above 650 typically unlock competitive terms, as the system weighs FICO equivalents against on-chain repayment history. Privacy stacks like zero-knowledge proofs safeguard sensitive inputs, ensuring compliance without data leaks.

Step-by-Step Onboarding to 3Jane Protocol

Unlock Collateral-Free USDC: Borrow Against TradFi Credit in 4 Steps

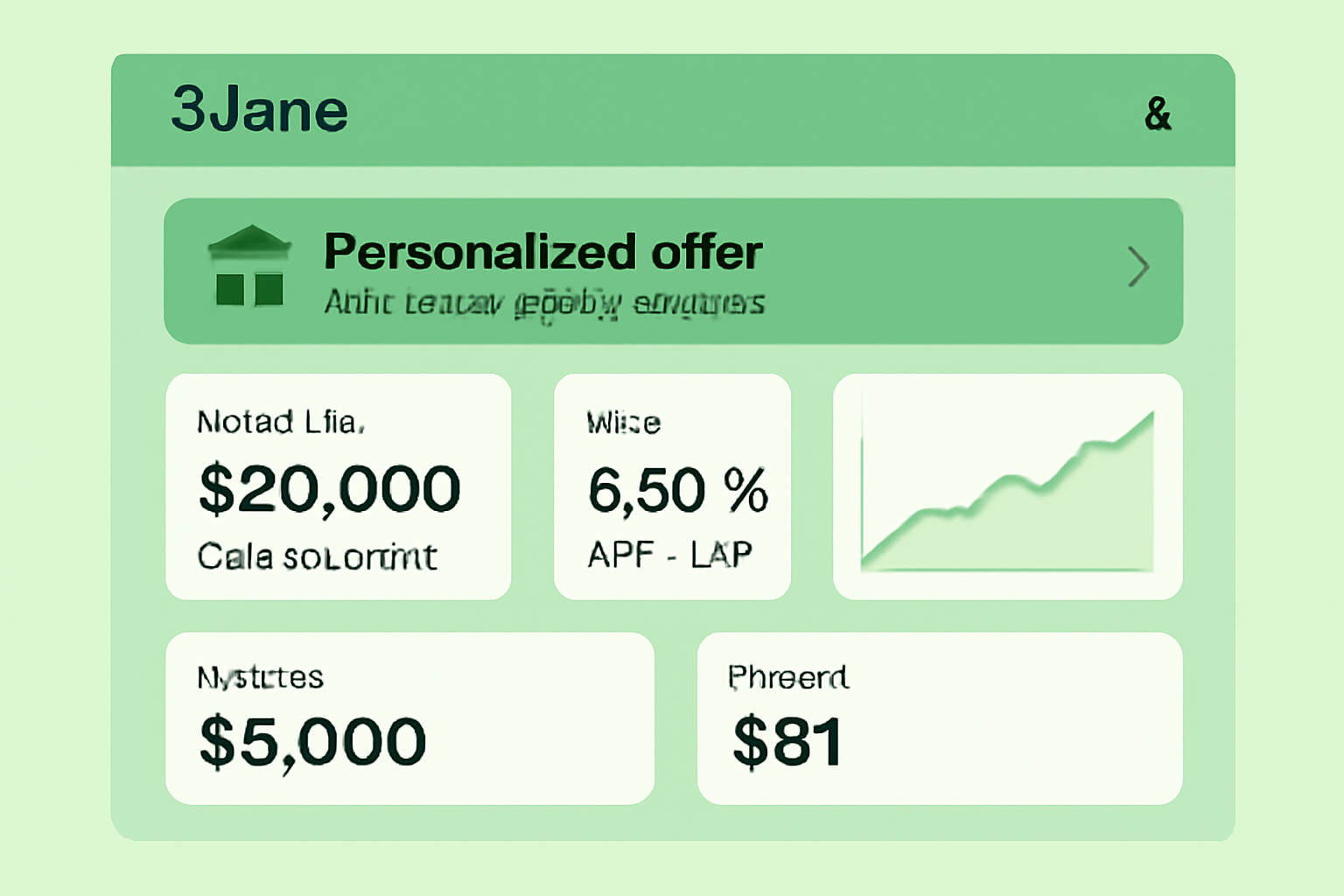

The onboarding process begins at the 3Jane interface, where wallet connection triggers a secure session. Plaid integration, a staple in fintech, verifies bank assets instantaneously, feeding into the underwriting engine alongside public blockchain proofs of prior DeFi activity. Consent for credit assessment is granular; users select data scopes to balance transparency and privacy. Within minutes, the dashboard displays a tailored offer: maximum borrowable USDC, APR, and duration, often up to $50,000 for qualified profiles.

Reviewing terms demands precision. Interest accrues daily on outstanding balances, with no hidden fees beyond gas costs. The protocol's whitepaper outlines algorithmic rate models, factoring volatility-adjusted credit multipliers. For instance, a borrower with strong TradFi history but nascent on-chain presence might secure 12% APR on a $10,000 line, repayable over 30-90 days.

Navigating Credit Assessment Nuances

3Jane's edge lies in its hybrid data fusion. Traditional scores provide baseline reliability, augmented by on-chain metrics like repayment velocity and asset diversity. This TradFi credit DeFi synergy unlocks trillions in sidelined capital, as undercollateralized products scale liquidity without liquidation cascades. Yet, borrowers must monitor oracle updates; discrepancies in off-chain feeds can adjust limits dynamically. Proactive repayment builds protocol-native credit graphs, lowering future rates and expanding access to advanced pools.

Security underpins viability. Audited smart contracts handle disbursements, with timelocks on defaults triggering reputational penalties over forced liquidations. This incentivizes adherence, fostering a self-sustaining ecosystem where trust emerges from verifiable behaviors across chains and ledgers.

Repayment mechanics further distinguish 3Jane's crypto borrowing no collateral framework. Once funds hit your wallet, automated streams deduct principal and interest from linked sources or on-chain balances, minimizing default risks through predictive modeling. Missed payments escalate via soft penalties first, higher rates or reduced limits, before harder measures like credit graph downgrades. This graduated enforcement mirrors TradFi grace periods but executes immutably on-chain, building a persistent reputation score transferable across DeFi protocols.

Risks and Mitigation Strategies in Undercollateralized Lending

While alluring, unsecured loans carry inherent volatilities. Off-chain data feeds, reliant on oracles like Chainlink, introduce oracle risk; a delayed bank balance sync could temporarily cap your line. Borrowers with thin on-chain history face steeper scrutiny, as the protocol prioritizes hybrid signals over isolated TradFi scores. My analysis of similar pilots reveals default rates hovering at 2-5%, far below CeFi unsecured benchmarks, thanks to real-time behavioral scoring.

Collateralized (Aave/Compound) vs Undercollateralized (3Jane) Comparison

| Aspect | Collateralized (Aave/Compound) | Undercollateralized (3Jane) |

|---|---|---|

| Collateral Ratio | 150-300% ❌ (Capital locked) | 0% ✅ (No collateral required) |

| Interest Rates | Market-driven, lower (2-10%) ✅ | Credit-based, higher (8-27%) ❌ |

| Liquidation Risk | High 📉 (Volatility-triggered) | Low/none 🔒 (Underwritten by credit) |

| Accessibility | Limited to crypto holders 🔒 | Broad, TradFi credit scores 🌐 |

| Capital Efficiency | Low ❌ (Overcollateralized) | High ✅ (Frees up capital) |

To mitigate, diversify data inputs: maintain active DeFi positions and consistent bank flows. Platforms embed circuit breakers, pausing disbursements during market stress, ensuring lender solvency. As a strategist, I advocate stress-testing your profile via the dashboard simulator before borrowing, input hypothetical downturns to gauge limit resilience.

Maximizing Benefits of 3Jane Borrow USDC

Leveraging this setup unlocks compounding advantages. Borrow USDC at 10% APR, deploy into stable yield pools earning 15%, netting positive carry while preserving TradFi credit intact. For developers, these lines fund payroll or liquidity bootstraps without diluting tokens. The protocol's privacy compliance stack, zero-knowledge proofs over credit multipliers, sidesteps KYC dragnets, appealing to global users wary of surveillance.

Paradigm's backing signals conviction; their thesis posits undercollateralized markets absorbing trillions from sidelined TradFi liquidity. Early metrics bear this out: TVL growth from seed pools to $50M and within quarters, with borrower retention above 80% due to dynamic incentives like loyalty multipliers.

Opinionated take: traditional collateral prisons stifled DeFi's potential; 3Jane's fusion liberates it, albeit with disciplined underwriting. Borrowers who treat this as a precision tool, not a free lunch, thrive, forging credit histories that span ledgers. Lenders, meanwhile, capture yields untethered to crypto betas, diversifying beyond LSTs.

This on-chain evolution demands vigilance: audit reports, though rigorous, can't eliminate novel exploits. Yet, the yield-risk arbitrage favors early adopters. As Ethereum scales via L2s, expect 3Jane iterations to deepen oracle diversity, incorporating payroll streams and invoice factoring for even richer profiles. The result? A credit bureau reborn on blockchain, where TradFi credit DeFi convergence propels inclusive finance forward, one verified score at a time.

No comments yet. Be the first to share your thoughts!