In 2025, the decentralized finance (DeFi) landscape is undergoing a seismic shift as on-chain credit scoring emerges as the linchpin for undercollateralized crypto loans. Unlike traditional DeFi lending, which demands borrowers lock up assets far exceeding their loan value, on-chain credit assessment harnesses blockchain data to gauge trustworthiness directly. This innovation is not only boosting capital efficiency but also opening the doors of DeFi to a broader swath of users, many of whom previously lacked sufficient collateral to participate.

From Overcollateralization to Capital Efficiency

The early days of DeFi lending were defined by overcollateralization: to borrow $1,000 worth of stablecoins, users might have needed to deposit $1,500 or more in crypto assets. This model protected lenders but severely limited access and capital utilization. In 2025, on-chain credit scoring is rewriting these rules by analyzing wallet activity, transaction histories, smart contract interactions, repayments, to produce a dynamic risk profile for every address.

This shift is already visible in market data: on-chain collateralized loans surged 42% in Q2 2025 and reached $26.5 billion in outstanding volume (CoinLaw). Yet the true breakthrough lies in protocols now offering undercollateralized loans, leveraging blockchain reputation rather than static asset balances. By tying scores to wallet addresses instead of personal identities, these systems preserve user privacy while unlocking trillions in new lending potential (Onchain). For a deep dive into how these risk scores underpin undercollateralized lending models, see this resource.

The Mechanics of On-Chain Credit Assessment

How do protocols actually compute a trustworthy credit score from on-chain data? The process involves aggregating multiple signals, such as wallet age, transaction frequency, historical loan performance, and even participation in governance or staking pools. Machine learning models (like those deployed by RociFi Labs) ingest this granular data, outputting non-fungible credit scores that can be referenced by any lender or protocol.

Smart contracts then use these scores to automate loan terms. If your score improves through timely repayments or increased activity across reputable dApps, you might receive lower interest rates or reduced collateral requirements, without any manual review process. This automation not only streamlines lending operations but also incentivizes positive borrower behavior.

The Rise of Decentralized Credit Bureaus and Protocol Interoperability

A key development fueling this transformation is the emergence of decentralized credit bureaus. These platforms aggregate reputation signals across chains and protocols using open-source frameworks. The result? Your borrowing reputation becomes portable, you can access favorable terms on multiple platforms without rebuilding your history from scratch.

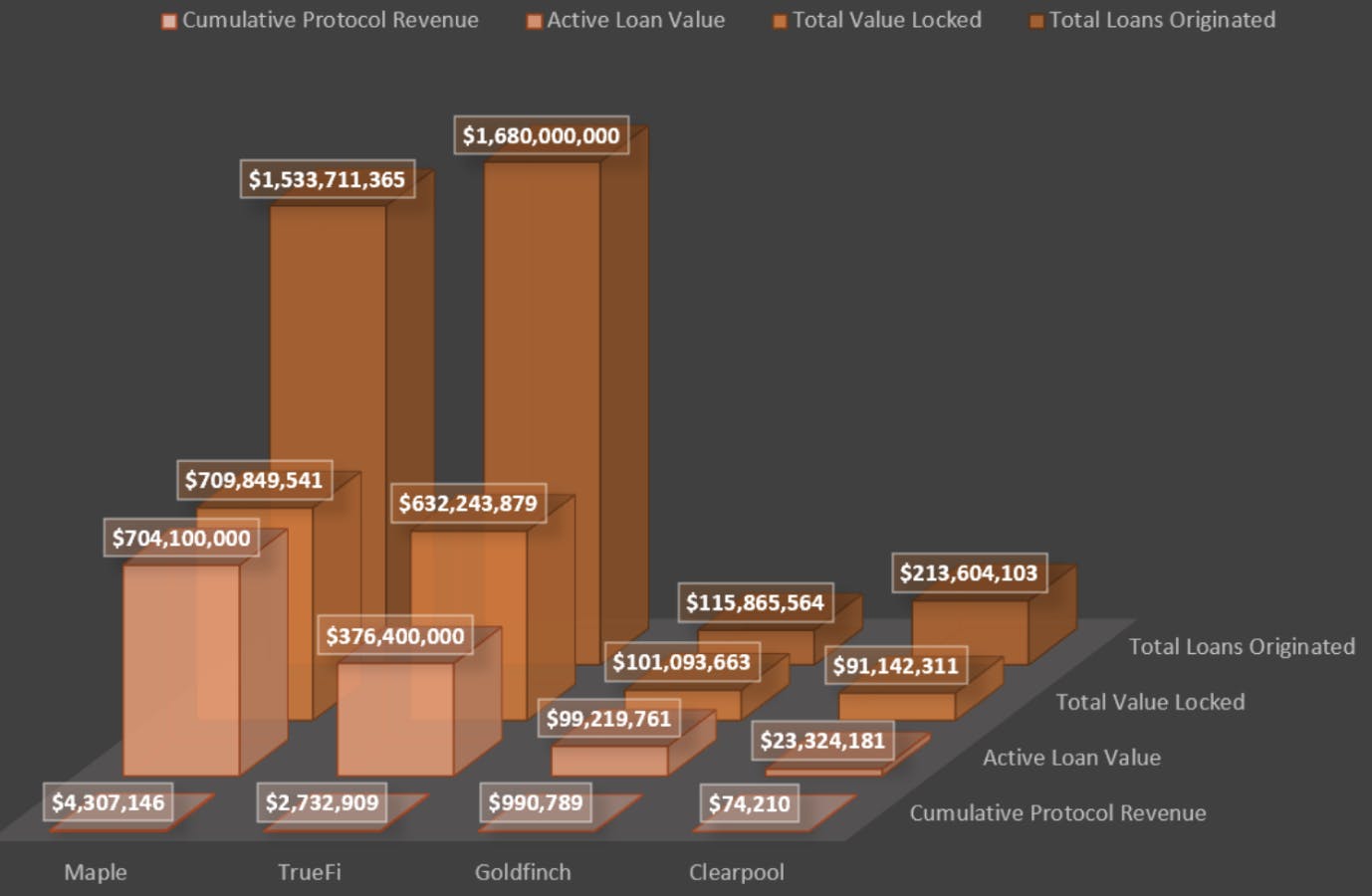

This interoperability is vital for scaling undercollateralized lending pools safely. For example, Goldfinch connects crypto liquidity providers with off-chain credit assessments for real-world borrowers; Maple Finance empowers professional delegates to vet institutional borrowers before issuing undercollateralized loans via smart contracts; TrueFi combines community voting with transparent on-chain scoring for unsecured lending (Mitosis University). Each approach demonstrates the growing sophistication and composability of blockchain reputation systems.

Bridging TradFi Standards with Blockchain Transparency

The integration between traditional finance (TradFi) standards and blockchain-native mechanisms is accelerating adoption among institutional players. Notably, Untangled Finance’s partnership with Moody’s Ratings brings established credit ratings onto public blockchains using zero-knowledge proofs, allowing secure publication and updates without sacrificing privacy (Coindesk). This hybrid approach enhances transparency while retaining regulatory-grade risk assessment standards.

Taken together, these advances signal that on-chain risk scores are rapidly transforming undercollateralized crypto lending. As protocols move toward real-time adjustments and composable reputations across platforms, DeFi is poised to rival traditional banking in both efficiency and accessibility.

Today, the interplay between on-chain credit scoring and protocol design is fostering a new era of trust-minimized lending. By shifting the underwriting process from opaque, centralized gatekeepers to transparent blockchain analytics, DeFi platforms now offer a spectrum of loan products tailored to nuanced risk profiles. This democratization of credit assessment is especially significant for users in emerging markets or those excluded from legacy financial systems.

Lenders benefit from granular risk segmentation and real-time monitoring, while borrowers gain access to capital with terms that reflect their actual on-chain behavior, not just their ability to overcollateralize. As borrowers build positive repayment histories on-chain, their scores improve, unlocking lower interest rates and larger borrowing limits across interoperable protocols. This feedback loop rewards responsible participation and strengthens the overall ecosystem.

- Privacy-preserving reputation: Scores are tied to wallet addresses rather than personal identities, ensuring privacy while maintaining accountability.

- Dynamic risk adjustment: Smart contracts update terms in real time based on evolving credit data.

- Ecosystem-wide portability: Credit reputations can be leveraged across multiple DeFi protocols and chains.

- Reduced systemic risk: Transparent scoring frameworks help lenders avoid concentrated exposures and identify emerging risks early.

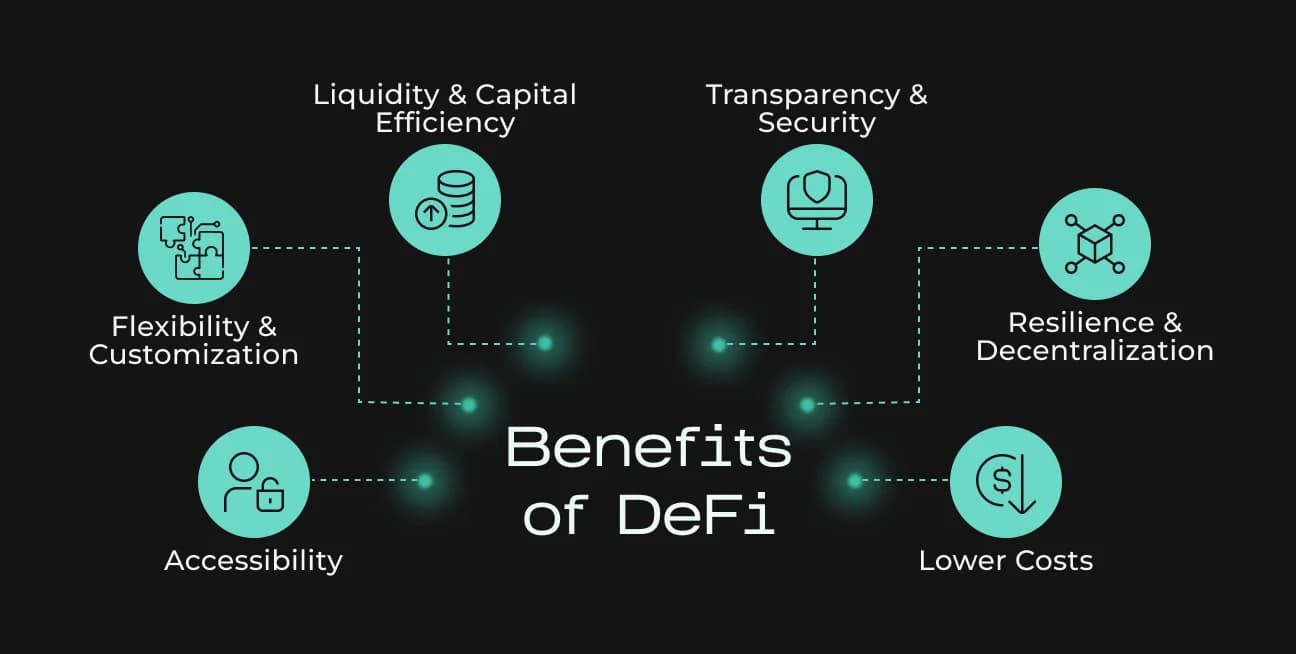

Key Benefits of On-Chain Credit-Backed Undercollateralized Crypto Loans

- Enhanced Capital Efficiency: On-chain credit scoring enables borrowers to access loans with less or no collateral, freeing up capital for other investments and boosting overall liquidity in DeFi markets.

- Broader Access to Credit: By assessing wallet-based reputations, protocols like Goldfinch and TrueFi allow users without large crypto holdings to obtain loans, expanding financial inclusion globally.

- Automated, Real-Time Risk Management: Smart contracts use on-chain credit scores to dynamically adjust loan terms, interest rates, and collateral requirements, improving both borrower experience and lender security.

- Privacy-Preserving Reputation: Credit scores are tied to wallet addresses, not personal identities, maintaining user privacy while enabling trustless lending.

- Interoperable and Portable Credit Profiles: Decentralized credit bureaus standardize on-chain reputation, allowing users to leverage their creditworthiness across multiple DeFi protocols and blockchains.

- Bridging Traditional and Decentralized Finance: Integrations like Untangled Finance and Moody’s Ratings bring established credit ratings on-chain, enhancing transparency and facilitating institutional participation in DeFi lending.

- Transparent and Auditable Loan Processes: All loan data and credit assessments are recorded on-chain, ensuring full transparency and enabling independent verification by any participant.

Challenges and Regulatory Trends in 2025

The path forward is not without hurdles. Ensuring data integrity, so that scores cannot be gamed or manipulated, remains a critical challenge. Projects are increasingly experimenting with attestation layers (such as Ethereum Attestation Service) and decentralized identity standards to anchor reputation data credibly. Meanwhile, regulators are taking note: initiatives like MiCA in Europe and evolving FCA guidelines signal that robust compliance frameworks will be essential for long-term growth (galaxy. com). The convergence of regulatory clarity with technical innovation could catalyze even broader adoption among institutional lenders seeking compliant exposure to DeFi yields.

The question of user privacy also looms large. Zero-knowledge proof (ZKP) technology is gaining traction as a way to prove creditworthiness without revealing sensitive transaction details. This cryptographic approach enables both compliance and confidentiality, a dual mandate for next-generation decentralized credit bureaus.

What’s Next: The Road to Trillions in On-Chain Lending

The momentum behind undercollateralized crypto lending is undeniable. With over $35 billion in active loans recorded by mid-2025 (Hackernoon) and major protocols like Aave and Compound continuing to dominate volume, the market’s trajectory points toward exponential growth as credit assessment infrastructure matures. As more capital enters DeFi through both retail wallets and institutional channels, expect further innovation at the intersection of machine learning, decentralized identity, and regulatory technology.

The ultimate vision? A global financial system where anyone with a blockchain wallet, and a verifiable history of responsible participation, can access fair, efficient capital markets without intermediaries or arbitrary barriers. For more technical insights into how these systems work under the hood, see this guide on risk scores powering undercollateralized lending in DeFi.

The coming years will test which models deliver sustainable yield while managing default risk transparently, but if current trends hold, on-chain credit scoring will remain at the core of DeFi’s evolution from speculative playground to mainstream financial infrastructure.

No comments yet. Be the first to share your thoughts!