In 2025, the decentralized finance (DeFi) landscape is undergoing a seismic shift as on-chain credit scores unlock the next evolution of lending: uncollateralized loans. Traditionally, DeFi lending has been dominated by overcollateralized models, where borrowers must deposit more value than they wish to borrow. This approach, while effective for risk management, has limited capital efficiency and excluded many potential borrowers from participating in the ecosystem. The advent of blockchain reputation scoring is now changing that dynamic.

From Overcollateralization to Reputation-Based Lending

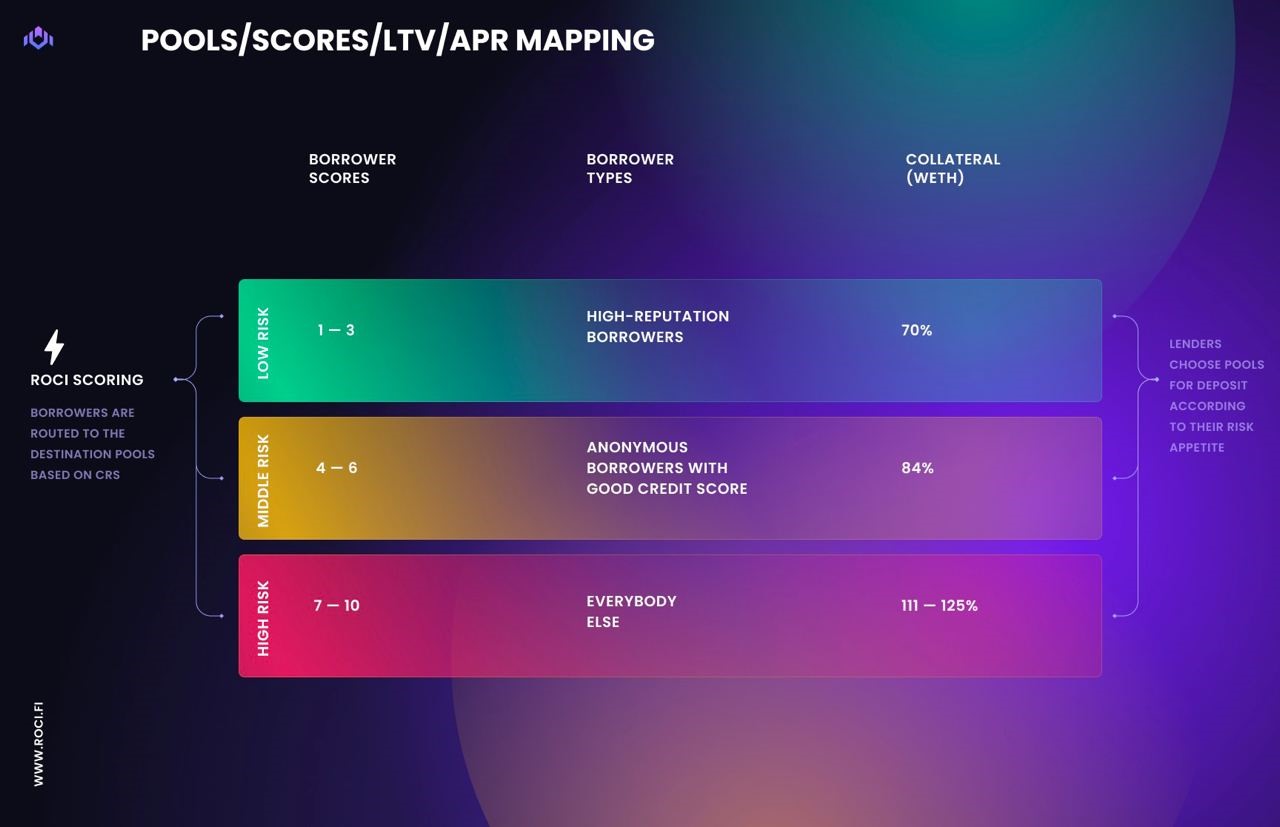

The core innovation driving this transformation is the ability to assess a user’s creditworthiness directly on-chain. By analyzing transaction patterns, repayment histories, protocol interactions, and even off-chain data (thanks to zero-knowledge proofs), DeFi credit protocols in 2025 can construct a robust picture of borrower reliability. These privacy-preserving credit assessments enable platforms to extend loans without requiring massive collateral buffers.

This paradigm shift is not merely theoretical. In August 2025 alone, onchain lending venues like Aave and Compound accounted for nearly 90% of DeFi volume (source). However, it’s the newer wave of undercollateralized protocols - such as 3Jane, Goldfinch, and Maple Finance - that are pushing boundaries by utilizing advanced Web3 credit score models. These platforms are demonstrating that risk can be managed through transparent data analytics rather than blunt collateral requirements.

The Mechanics Behind On-Chain Credit Scoring

How exactly do these systems work? At their core, on-chain credit scores aggregate and analyze a user’s entire blockchain financial footprint. Key metrics include:

- Repayment history: Has the user reliably paid back previous loans?

- Asset holdings: What stablecoins or tokens does the wallet control?

- Diversity and frequency of transactions: Is the user active across multiple protocols?

- Engagement with DeFi primitives: Participation in liquidity pools, staking contracts, or DAOs.

The integration of off-chain data is also accelerating thanks to innovations like zero-knowledge proof technology. For example, Untangled Finance recently partnered with Moody’s Ratings to demonstrate how traditional credit ratings can be securely imported onto blockchains without compromising privacy. This fusion creates a holistic risk profile - one that is both comprehensive and resistant to manipulation.

Pioneers in Undercollateralized Lending: Protocols Leading the Charge

A few standout platforms are defining best practices for DeFi undercollateralized lending. The Ethereum-based 3Jane Protocol, for instance, underwrites unsecured lines of credit using both on-chain reputation scoring and off-chain financial proofs. Borrowers’ Jane Scores blend crypto wallet activity with verifiable documentation of assets or cash flows.

Goldfinch, meanwhile, connects crypto liquidity providers with real-world borrowers such as small businesses in emerging markets. Here, trusted partners perform due diligence and feed their assessments into smart contracts that automate loan origination and repayment - all visible on chain for maximum transparency.

Maple Finance employs decentralized groups of professional underwriters who analyze loan requests off-chain but execute funding via smart contracts. This model allows vetted crypto-native companies to access capital efficiently while maintaining rigorous risk controls.

These pioneering protocols are not only expanding the boundaries of what is possible in DeFi but are also attracting traditional financial players. The integration of Web3 credit scores with off-chain data has caught the attention of institutional lenders, who now see blockchain-based reputation scoring as a viable risk mitigation tool. This convergence is accelerating capital inflows and diversifying borrower profiles well beyond the early crypto-native audience.

Opportunities and Risks in Uncollateralized DeFi Lending

While uncollateralized DeFi loans offer transformative potential, they also introduce new complexities and risks. The transparency of on-chain activity provides lenders with an unprecedented level of insight, but it also raises concerns around privacy and data sovereignty. Moreover, the absence of collateral means that protocols must rely heavily on the accuracy and integrity of their credit models.

To illustrate the current landscape, consider the following comparative overview of leading undercollateralized lending platforms:

Comparison of DeFi Uncollateralized Lending Platforms (2025)

| Platform | Credit Model | Loan Volume (2025) | Default Rate (2025) |

|---|---|---|---|

| 3Jane | On-chain & off-chain credit scoring (Jane Score), verifiable proofs of assets and cash flows | $1.2B | 2.1% |

| Goldfinch | Off-chain credit assessment by trusted partners, on-chain loan execution | $950M | 3.8% |

| Maple Finance | Pool-delegate model, off-chain due diligence, on-chain lending to crypto-native companies | $1.5B | 1.7% |

The table highlights that while default rates remain low for borrowers with high on-chain scores, platforms continue to iterate on their risk controls. Innovations such as real-time credit monitoring and automated liquidation triggers are being deployed to further reduce losses. Notably, these advances are enabling DeFi to rival - and in some cases surpass - traditional finance in both speed and transparency.

What’s Next for Blockchain Reputation Scoring?

The next phase for DeFi credit protocols 2025 will center on interoperability and standardization. As more platforms adopt privacy-preserving credit assessment tools, we can expect greater portability of reputation across protocols. This means that a strong borrowing history on one platform could unlock preferential terms elsewhere, a true network effect for Web3 users.

The regulatory outlook remains fluid. Some jurisdictions are beginning to recognize decentralized credit markets as legitimate financial infrastructure, while others continue to debate compliance standards around anti-money laundering (AML) and know-your-customer (KYC) requirements. What is clear: as adoption grows, so too will efforts to harmonize rules without sacrificing user autonomy or privacy.

How Users Can Benefit from On-Chain Credit Scores

For individuals and businesses alike, the rise of blockchain reputation scoring opens up new opportunities:

- Access to capital: Borrowers without large crypto holdings can secure loans based on their demonstrated reliability.

- Lower borrowing costs: High-scoring users may enjoy reduced interest rates or flexible repayment terms.

- Financial sovereignty: Creditworthiness is determined by transparent algorithms rather than opaque institutions.

This shift toward algorithmic trust is already reshaping global lending patterns. As more users recognize the value of cultivating a positive Web3 credit score, competition among borrowers will drive further innovation in both risk modeling and product design.

The transition from overcollateralized to undercollateralized lending marks a watershed moment for decentralized finance. By leveraging transparent data analytics alongside privacy-preserving technologies, DeFi is poised to bring trillions in untapped value onto blockchains worldwide. For those ready to embrace this new paradigm, understanding how on-chain credit scores enable uncollateralized lending in DeFi will be essential for navigating both opportunity and risk in the years ahead.

No comments yet. Be the first to share your thoughts!