Decentralized Finance (DeFi) lending has exploded in popularity, but with opportunity comes risk. Unlike traditional banks that rely on credit bureaus and lengthy paperwork, DeFi lenders operate in a permissionless environment where anyone can request a loan. This innovation opens doors for millions yet introduces a core challenge: How do you assess borrower risk when identities are pseudonymous and collateral is often minimal?

Why DeFi Needs On-Chain Credit Scores

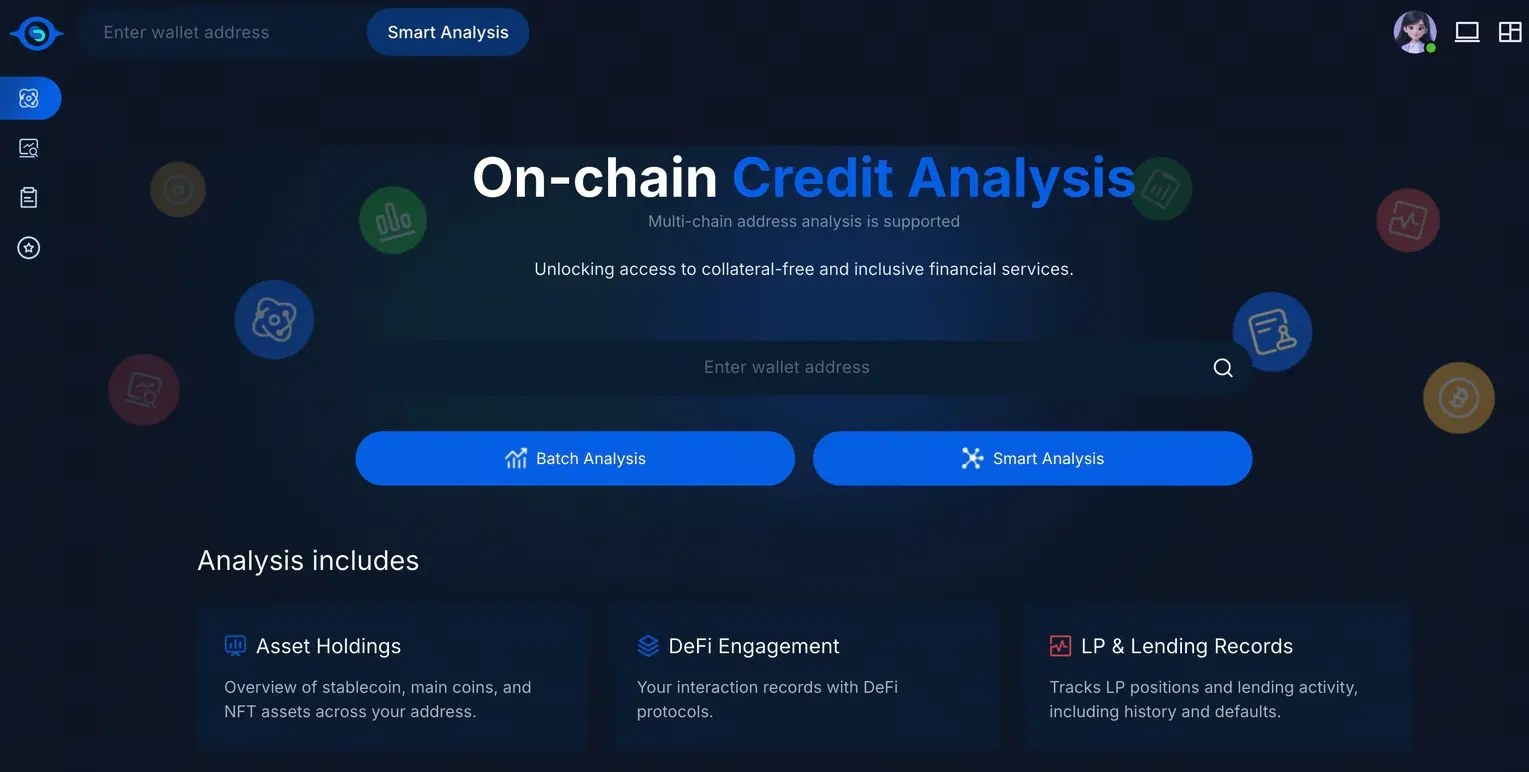

The answer lies in the evolution of on-chain credit scoring. Instead of sifting through pay stubs or FICO reports, DeFi protocols tap directly into blockchain data. Every wallet tells a story: transaction volumes, repayment history, protocol interactions, and yield farming patterns all leave an immutable trail. By harnessing this data, platforms can build comprehensive financial profiles for any address, without ever knowing the person behind it.

This approach isn’t just theoretical. Platforms like Trava Finance and Credefi are already leveraging these tools to reduce default rates and unlock new forms of lending. The result? More tailored loan terms, lower collateral requirements, and a much broader pool of eligible borrowers.

The Mechanics: How On-Chain Credit Scoring Works

On-chain credit scoring mechanisms use a blend of analytics and machine learning to translate raw blockchain activity into actionable risk scores:

- Transaction History Analysis: Every swap, borrow, or repayment is tracked on-chain. Lenders analyze this data to gauge reliability and spot risky behavior.

- AI-Powered Pattern Recognition: Advanced platforms employ artificial intelligence to detect subtle trends, like sudden spikes in leverage or repeated liquidations, that signal higher default risk.

- Decentralized Identity (DID) Integration: Borrowers can link verifiable digital identities to their wallets, providing richer context for risk assessment while preserving privacy.

This multifaceted approach gives lenders a real-time edge. Instead of static snapshots, they enjoy dynamic insights, enabling them to adjust interest rates or collateral requirements as borrower profiles evolve.

Case Studies: Real-World Impact Across DeFi Platforms

The impact is tangible across leading protocols:

- Credefi: By combining blockchain analytics with traditional data from agencies like Experian, Credefi dynamically adjusts loan conditions based on hybrid risk profiles, a fusion that slashes default rates while expanding access.

- Trava Finance: Trava’s cross-chain credit scoring lets users leverage their entire on-chain history for better borrowing terms. Lenders can set minimum score thresholds, directly reducing exposure to risky wallets.

This isn’t just about safety; it’s about efficiency. Accurate risk assessment means lower collateral requirements and more capital flowing through the ecosystem, a win-win for borrowers and lenders alike. For an in-depth look at how these innovations are transforming lending dynamics, check out our guide on how on-chain credit scores improve risk assessment for DeFi lending platforms.

The Benefits: Lower Defaults and Greater Inclusion

The results speak for themselves:

- Lenders enjoy reduced default rates, as real-time analytics catch red flags before loans are issued.

- Borrowers gain access to fairer terms, especially those without legacy credit histories but strong on-chain reputations.

- The ecosystem grows more resilient, with capital allocated efficiently based on transparent risk metrics rather than guesswork or exclusionary criteria.

On-chain credit scores are not just a technological upgrade, they’re a paradigm shift for DeFi lending risk assessment. By rooting decisions in transparent, immutable data, these systems help protocols sidestep many pitfalls that plagued early DeFi markets. Gone are the days when lenders had to over-collateralize every loan or rely on gut instinct to gauge risk. Now, creditworthiness is calculated with precision and fairness, using blockchain credit scoring as the backbone.

Top 3 Advantages of On-Chain Credit Scores for DeFi Lenders

- Reduced Collateral Requirements: On-chain credit scores allow DeFi lenders to accurately assess borrower risk, enabling lower collateral demands and making loans more accessible and capital-efficient. This empowers platforms like Credefi to offer flexible lending terms while maintaining security.

- Enhanced Risk Management: Real-time analysis of on-chain data enables dynamic risk assessment. Lenders can promptly adjust interest rates and loan terms based on evolving borrower profiles, significantly reducing the risk of defaults. Platforms such as Trava Finance exemplify this adaptive approach.

- Increased Financial Inclusion: By evaluating on-chain behavior instead of relying on traditional credit histories, DeFi lenders can extend credit to a broader range of users globally. This opens up financial opportunities for individuals previously excluded from the traditional banking system, driving true decentralization.

One of the most compelling aspects of this evolution is crypto loan default prevention. With AI and real-time analytics constantly monitoring wallet activity, lenders can proactively flag risky behavior, such as sudden asset withdrawals or repeated late repayments, before defaults occur. This dynamic adjustment empowers protocols to fine-tune interest rates or collateral demands instantly, making DeFi lending safer and more adaptive than ever before.

Privacy remains a core value in Web3 credit analytics. On-chain scores are generally tied to wallet addresses rather than personal identities, ensuring users retain control over their data while still building reputational capital. This balance between transparency and privacy is unlocking new waves of financial inclusion: users previously excluded from legacy systems due to lack of paperwork or geography can now access loans based on their blockchain track record alone.

The ripple effects extend beyond individual platforms. As more protocols adopt standardized on-chain credit scores, the entire Web3 ecosystem benefits from increased interoperability and trust. Lenders can compare risk across different protocols with greater confidence, while borrowers gain portable reputations that travel with them from one dApp to another, a true leap forward for decentralized finance.

Curious how under-collateralized lending is becoming possible thanks to these advances? Explore our resource on how on-chain risk scores enable under-collateralized lending in DeFi for deeper insights into this game-changing trend.

Looking Ahead: The Future of Risk Management in DeFi

The momentum behind on-chain credit innovation shows no sign of slowing down. As machine learning models grow more sophisticated and cross-chain analytics become standard, expect even sharper differentiation between high- and low-risk borrowers. Lenders will continue to refine their offerings, think dynamic loan terms that evolve with your reputation, and borrowers will have unprecedented agency over their financial destinies.

This new era isn’t just about reducing defaults; it’s about building a more open, efficient, and equitable financial system for all participants. For those ready to seize opportunity in the next wave of decentralized lending, understanding and leveraging on-chain credit scores isn’t optional, it’s essential.

No comments yet. Be the first to share your thoughts!