DeFi lending is on the verge of a seismic shift. For years, the lack of reliable on-chain credit scores forced borrowers to lock up mountains of collateral just to access capital. This model excluded millions and kept DeFi’s capital efficiency stuck in first gear. But that’s changing fast. With Ethereum (ETH) currently trading at $4,037.50, the market’s appetite for innovation is growing - and on-chain credit scoring is about to unlock a trillion-dollar opportunity.

Why On-Chain Credit Scores Are a Game Changer for Uncollateralized DeFi Loans

Traditional lending relies on credit bureaus and opaque data silos. In DeFi, everything is transparent, but until recently, there was no way to translate raw blockchain activity into a meaningful credit score. Enter on-chain credit scoring: a system that analyzes your blockchain history, DeFi interactions, and repayment behavior to calculate your risk profile. This isn’t just theory - it’s fueling a new wave of uncollateralized and undercollateralized loans across the ecosystem.

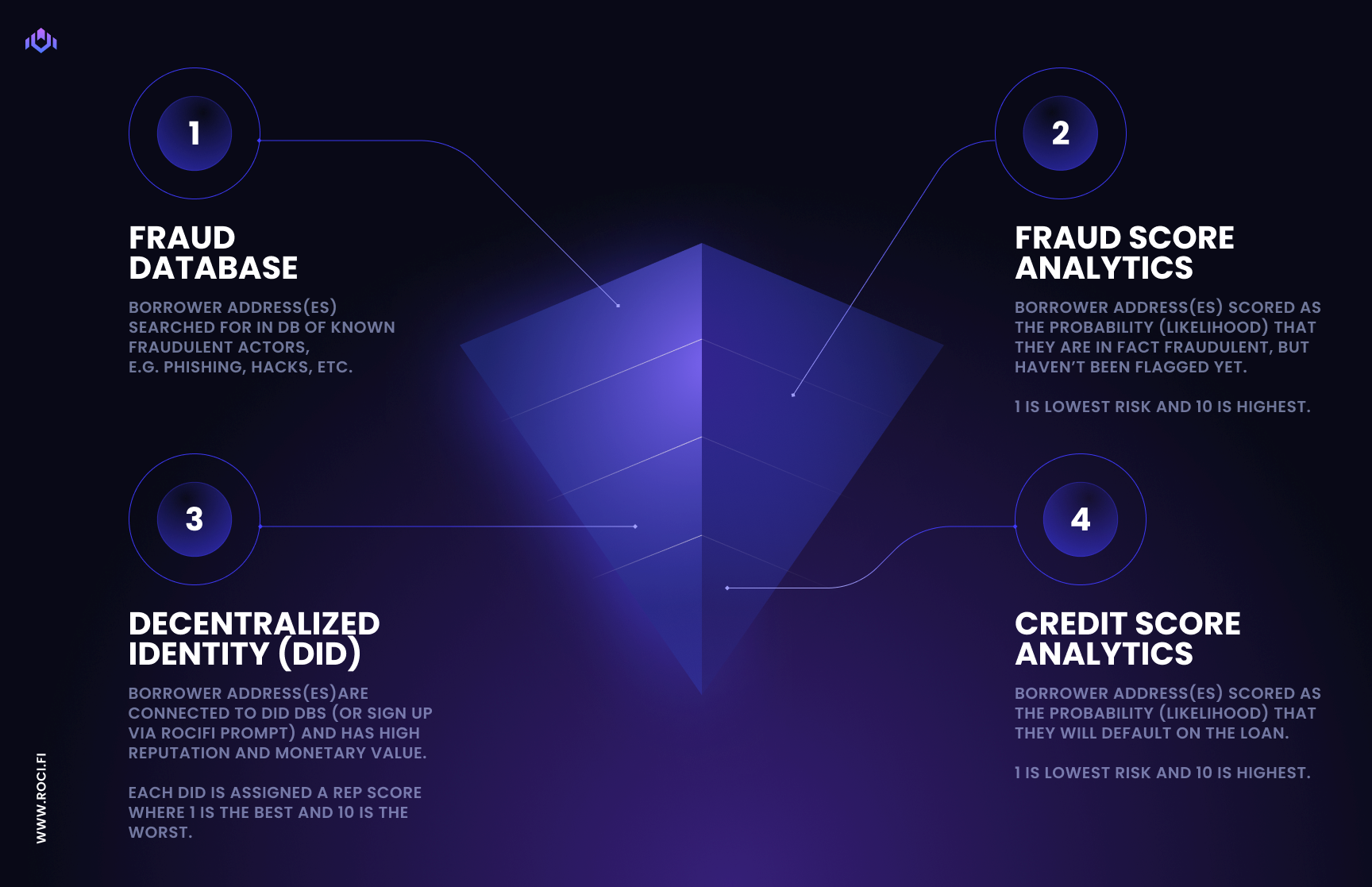

Protocols like Spectral Finance are pioneering Multi-Asset Credit Risk Oracles (MACRO scores), evaluating factors like borrowing behavior, liquidation history, and credit mix. Scores typically range from 300 to 850, echoing the familiar FICO model but built for the crypto-native world. Meanwhile, RociFi mints Non-Fungible Credit Scores (NFCS) as non-transferable tokens, encapsulating your DeFi reputation and decentralized identity. These innovations are making it possible for users with strong on-chain track records to borrow with little or no collateral for the first time.

"On-chain credit scores will bring trillions of dollars to DeFi by unlocking capital efficiency and trust. "

How Blockchain Credit Scoring Works: Data, Privacy, and Protocols

Let’s break down the mechanics. First, on-chain credit scoring systems aggregate your transaction history, lending activity, and protocol interactions. This data is publicly verifiable, ensuring transparency and eliminating the need for third-party trust. But privacy is still paramount. Solutions like Chainlink’s DECO protocol use zero-knowledge proofs to confirm off-chain data (think bank balances or traditional credit scores) without revealing sensitive details on-chain.

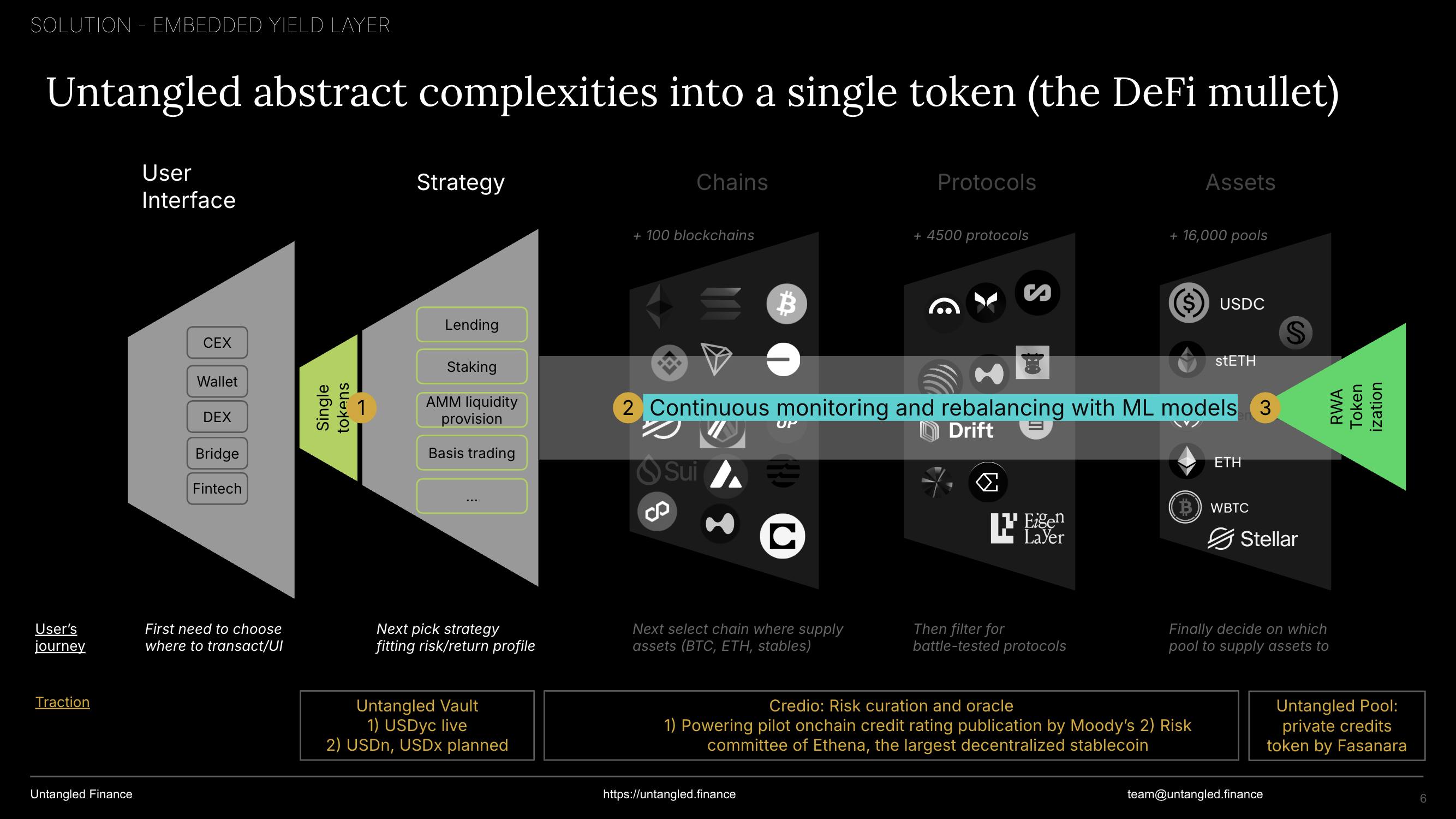

Other protocols are bridging the gap between off-chain and on-chain identity. For example, Untangled Finance and Moody’s have tested integrating legacy credit ratings with blockchain-based credentials, all while preserving user privacy through zero-knowledge proof technology. The result? A hybrid DeFi reputation system that’s both secure and censorship-resistant.

Top 5 Benefits of On-Chain Credit Scores in DeFi

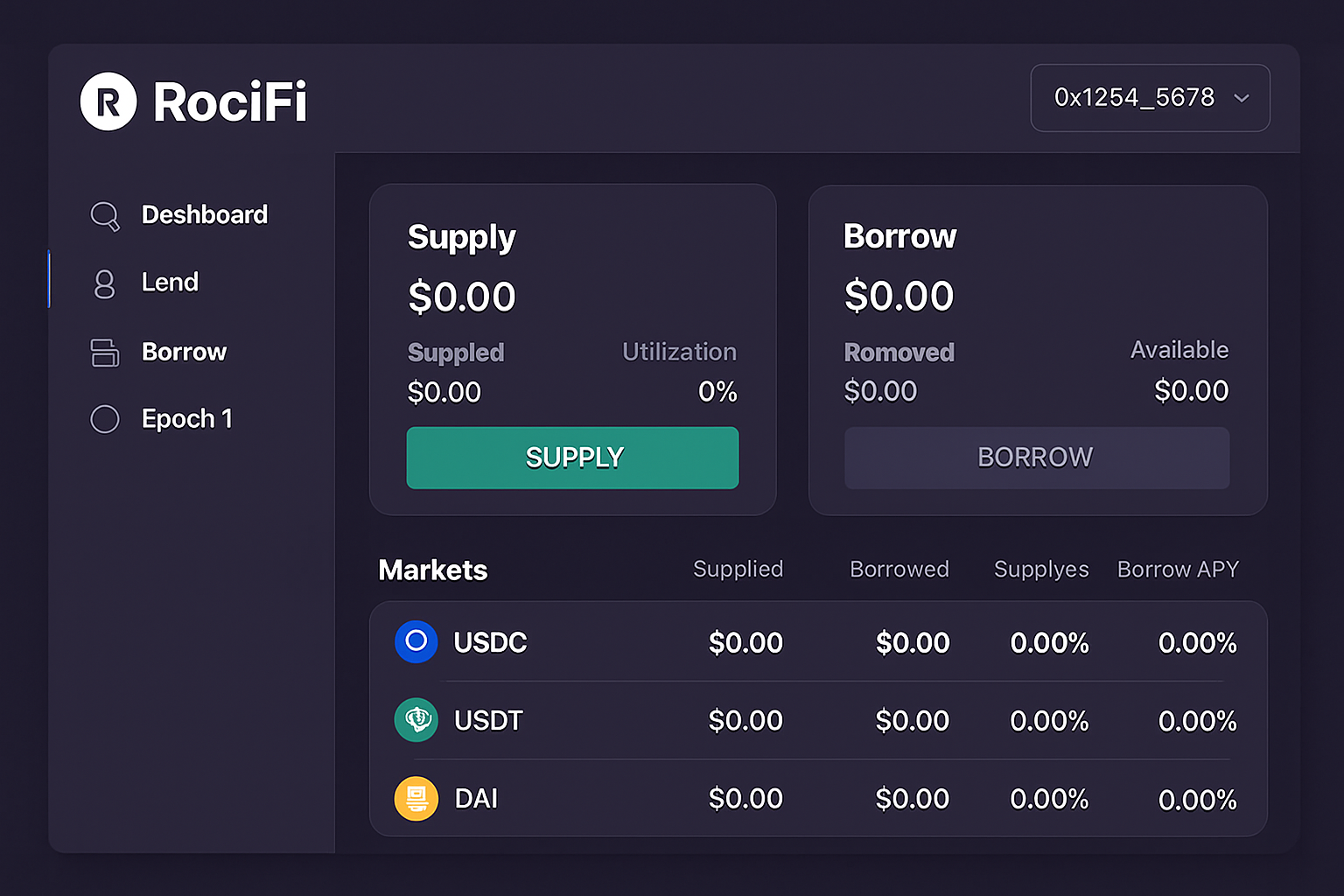

- Unlocks Uncollateralized Loans: On-chain credit scores enable DeFi protocols like RociFi and zScore to offer loans without requiring users to over-collateralize, making borrowing accessible to more participants.

- Promotes Financial Inclusion: By analyzing blockchain activity instead of traditional credit reports, on-chain scores allow users without a conventional credit history to access DeFi lending platforms, broadening global access to financial services.

- Boosts Capital Efficiency: Reducing or eliminating collateral requirements lets borrowers leverage their assets more effectively, increasing the overall capital efficiency within the DeFi ecosystem.

- Ensures Transparency and Security: Credit assessments are recorded on the blockchain, providing an immutable and tamper-proof record that builds trust among lenders and borrowers.

- Protects Privacy with Advanced Tech: Protocols like Chainlink DECO and 3Jane use zero-knowledge proofs and zkTLS to verify creditworthiness without exposing sensitive user data, maintaining privacy while enabling trustless lending.

Protocols Leading the Charge: Real-World Examples

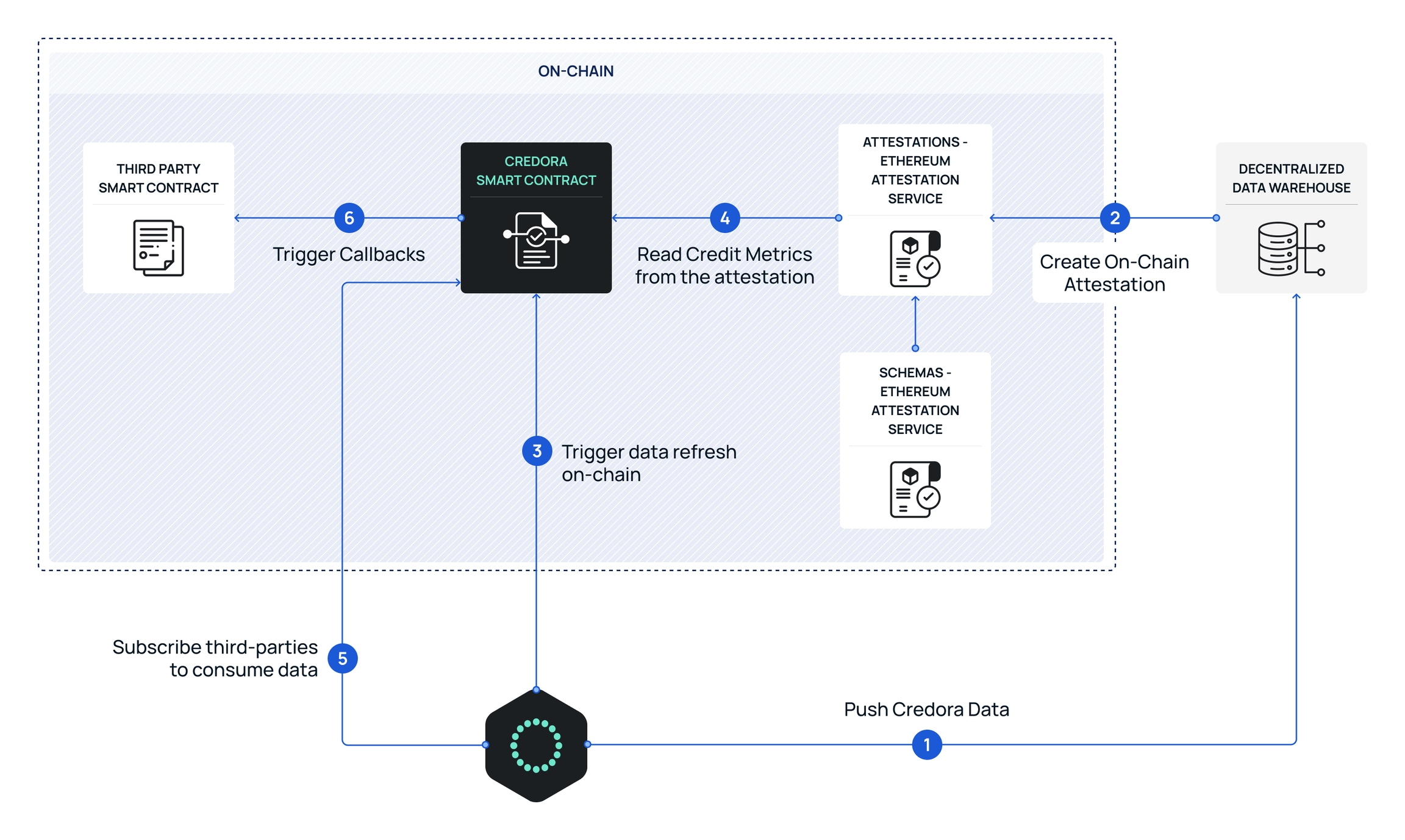

It’s not just theory - real protocols are already deploying on-chain credit scoring to power uncollateralized lending. Credora and Providence are calculating risk-adjusted returns for DeFi credit markets, giving lenders the tools to price risk more accurately. RociFi’s NFCS tokens are being adopted by lending platforms eager to extend credit based on blockchain reputation rather than just wallet balances.

Meanwhile, 3Jane is leveraging zkTLS technology to fuse off-chain and on-chain data, ensuring that only trustworthy users access loans. And with new solutions like EigenLayer’s zScore - a transferable, composable on-chain credit profile - DeFi is finally getting the infrastructure it needs to scale uncollateralized lending safely and efficiently.

From Reputation to Capital: What This Means for DeFi Borrowers

For users, the impact is massive. Instead of being penalized for not having traditional assets, your crypto credit history and DeFi reputation become your passport to financial opportunity. This is true financial inclusion: anyone with a track record of responsible on-chain activity can access capital without jumping through legacy hoops. The result? More efficient markets, lower barriers to entry, and a DeFi ecosystem that’s open to the world.

The ripple effects of on-chain credit scoring reach far beyond individual borrowers. For protocols, lenders, and the broader DeFi ecosystem, this innovation unlocks a new paradigm of risk management and capital deployment. Lenders can now price loans dynamically based on real-time, verifiable credit profiles, rather than relying on crude collateral ratios. Borrowers, in turn, can build portable reputations that follow them across platforms, creating a competitive marketplace for capital and driving down borrowing costs.

With Ethereum (ETH) holding steady at $4,037.50, the appetite for scalable, capital-efficient lending solutions is only intensifying. As more protocols integrate on-chain credit scores, expect to see an explosion of new lending products - from microloans for emerging markets to sophisticated undercollateralized credit lines for power users. The days of locking up 150% collateral just to get a loan are numbered.

"We’re witnessing the birth of a decentralized credit bureau. DeFi’s next wave will be powered by reputation, not just collateral. "

Challenges and Next Steps: Scaling Trust in a Borderless Ecosystem

Of course, there are hurdles to clear. On-chain credit scoring is only as robust as the data and models behind it. Sybil resistance, data fragmentation across chains, and the risk of gaming reputation systems remain open challenges. Privacy, too, is a moving target - zero-knowledge proofs are powerful, but adoption is still early and UX needs refinement.

Yet the momentum is undeniable. AI-powered analytics, as explored by Kava. io, are making credit models smarter and more adaptive. Spectral Finance’s MACRO scores and similar innovations are setting new standards for transparency and risk assessment in DeFi. As these tools mature, expect on-chain credit scores to become the backbone of permissionless lending, insurance, and even new asset classes.

What’s Next for Blockchain Credit Scoring?

The trajectory is clear: DeFi is moving from collateral-first to reputation-first. In the near future, your wallet’s on-chain credit score will be as important as your ETH balance. Expect to see more protocols integrating with decentralized identity solutions, cross-chain credit histories, and privacy-preserving data oracles. As uncollateralized DeFi loans become mainstream, capital will flow more freely, and the $4,037.50 ETH price could be just the beginning of a new growth cycle fueled by credit innovation.

Top DeFi Protocols Using On-Chain Credit Scores

- Spectral Finance – Pioneering on-chain credit scoring with its Multi-Asset Credit Risk Oracle (MACRO), Spectral assigns blockchain users a credit score (300–850) based on borrowing history, liquidations, and protocol interactions.

- RociFi – Issues Non-Fungible Credit Scores (NFCS) as non-transferable tokens, leveraging on-chain behavior and decentralized identity to enable undercollateralized lending.

- Untangled Finance – Integrates Moody’s credit ratings on-chain using zero-knowledge proofs, blending traditional and blockchain-based credit data for secure, privacy-preserving lending.

- 3Jane – Uses zkTLS technology to seamlessly connect on-chain and off-chain credit data, powering smart undercollateralized lending decisions.

- Credora – Provides real-time, on-chain credit scoring and risk analytics for DeFi lenders, helping assess borrower risk and unlock uncollateralized loan markets.

On-chain credit scores are more than a technical upgrade - they’re a catalyst for a more open, efficient, and inclusive financial system. For borrowers, lenders, and builders alike, the message is clear: reputation is the new collateral. Ride the wave, but always respect the risk.

No comments yet. Be the first to share your thoughts!