Decentralized finance (DeFi) has always promised an open, borderless alternative to traditional banking, but one foundational element has been missing: trust. Historically, DeFi lending protocols have sidestepped the issue of creditworthiness by demanding over-collateralization, often requiring users to lock up more value than they borrow. This approach, while secure for lenders, severely limits capital efficiency and excludes a vast cohort of potential borrowers. Enter decentralized credit scoring: a paradigm shift that is redefining how trust and risk are managed on-chain.

From Over-Collateralization to On-Chain Credit Reputation

The core challenge in DeFi lending has always been the absence of reliable, verifiable credit information. Without credit scores or reputation systems, protocols like Aave and Compound have defaulted to blunt risk controls, requiring borrowers to post collateral sometimes worth 150% or more of their loan. This model is safe but inefficient.

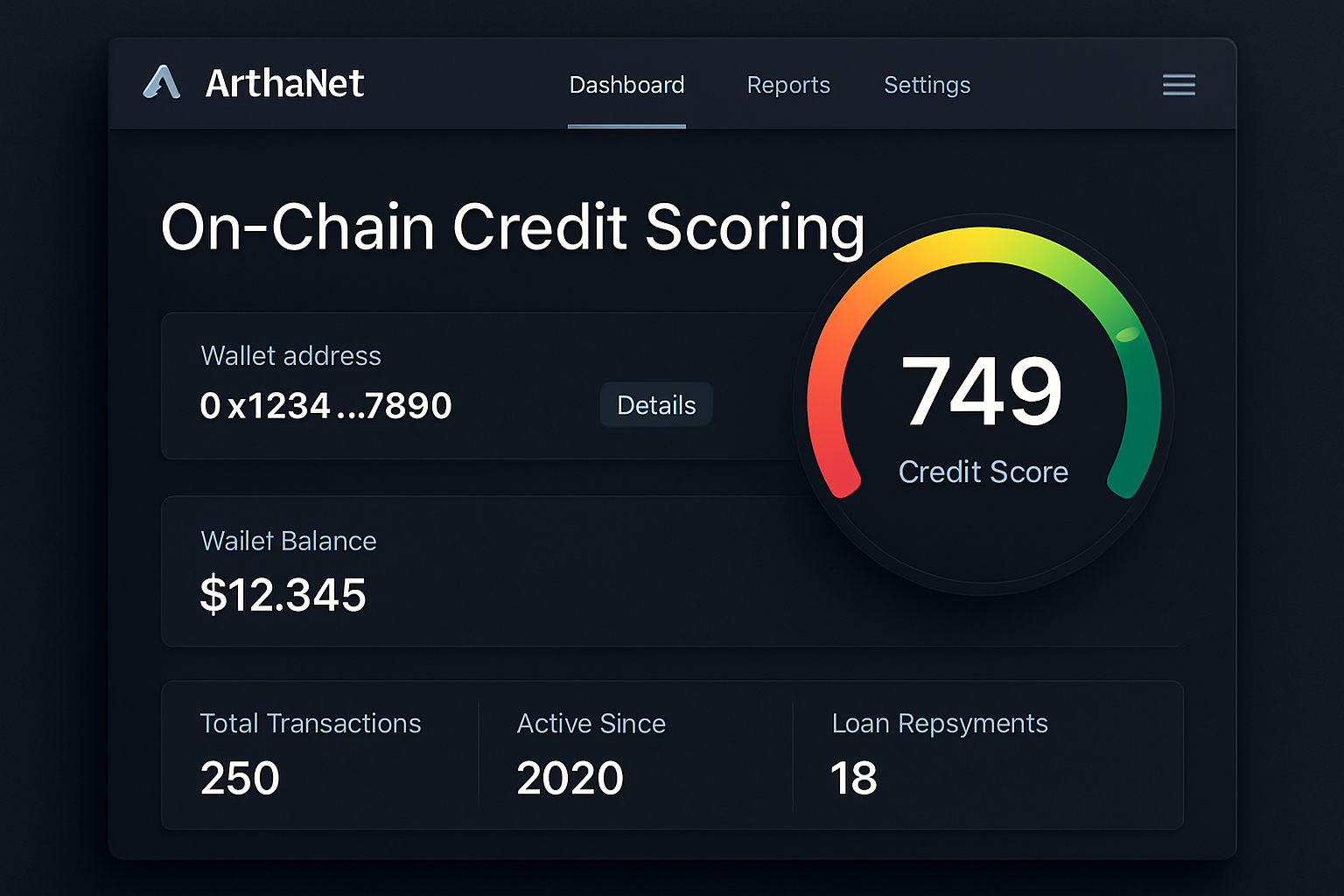

Now, innovative solutions such as the On-Chain Credit Risk Score (OCCR Score) are emerging to quantify credit risk based on wallet activity. By analyzing transaction histories, liquidity provision, repayment behavior, and participation in governance, these systems assign a blockchain credit score to every user. The result? Lenders can make risk-adjusted decisions, and borrowers with strong on-chain reputations can access loans with lower collateral requirements.

Key Benefits of On-Chain Credit Scoring in DeFi

-

Reduces Over-Collateralization: On-chain credit scoring platforms like ArthaNet allow DeFi protocols to assess borrower risk, enabling loans with lower collateral requirements and improving capital efficiency.

-

Enhances Transparency and Trust: Decentralized systems such as Spectral generate transparent, blockchain-verifiable credit scores, fostering greater trust between lenders and borrowers.

-

Integrates Traditional Credit Data: Initiatives from TransUnion and Untangled Finance with Moody’s Ratings bring real-world credit scores on-chain, bridging DeFi and traditional finance for more robust risk assessment.

-

Promotes Financial Inclusion: By leveraging on-chain activity rather than traditional financial history, decentralized credit scoring opens access to lending for users who are underbanked or lack conventional credit records.

How Decentralized Credit Scores Work

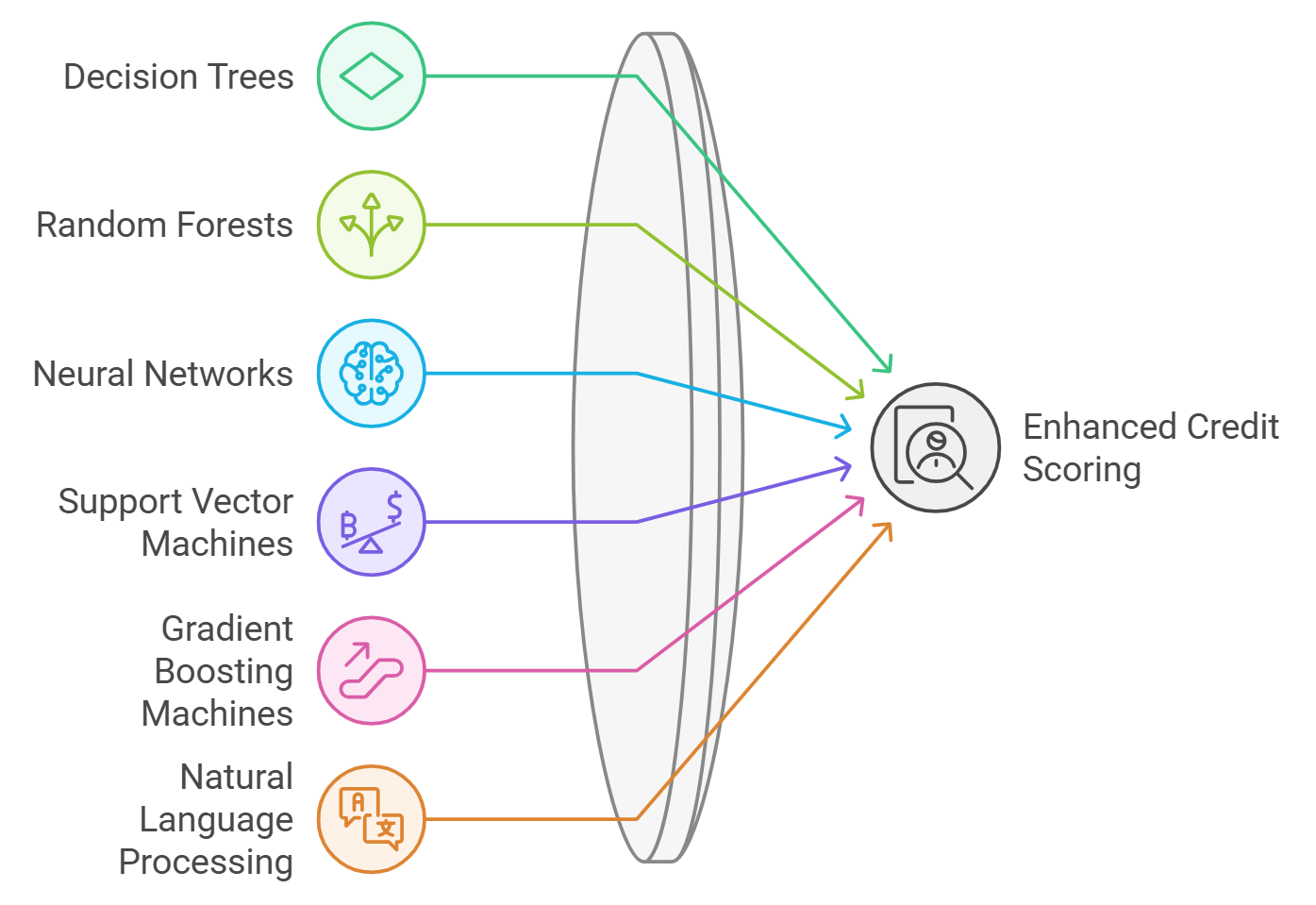

Modern decentralized credit scoring platforms leverage advanced analytics and machine learning to evaluate on-chain data. For example, ArthaNet’s system aggregates data across multiple blockchains, generating transparent and decentralized credit scores that are visible to users and protocols alike. Similarly, Spectral’s Multi-Asset Credit Risk Oracle (MACRO) issues Creditworthiness NFTs (cwNFTs), which encapsulate a user’s credit profile in a privacy-preserving format.

This evolution is not limited to purely crypto-native data. Untangled Finance’s pilot with Moody’s Ratings demonstrates how traditional credit data can be brought on-chain, allowing DeFi protocols to incorporate real-time credit insights without intermediaries. TransUnion’s partnership with blockchain platforms further bridges the gap between traditional and decentralized finance by allowing users to share their real-world credit scores when applying for DeFi loans.

Unlocking Capital Efficiency and Financial Inclusion

The implications of robust on-chain financial reputation systems are profound. By enabling undercollateralized or even unsecured lending, DeFi protocols can unlock capital that would otherwise remain idle. This not only boosts yields for lenders but also opens the door to underserved users who lack large crypto holdings but have demonstrated responsible on-chain behavior.

As decentralized credit scores become more sophisticated and widely adopted, we are witnessing a shift from trustless systems, where no one is trusted, to trust-minimized systems: where trust is earned and quantified on-chain. This transformation is creating new opportunities for both individuals and institutions within the DeFi ecosystem. For deeper insights into how these mechanisms are reshaping lending practices, see this analysis on reputation-based lending.

Key Players and Emerging Standards

The decentralized credit landscape is rapidly evolving, with platforms like Cred Protocol DeFi, ChainAware credit score, and others contributing to a vibrant ecosystem of risk assessment tools. These solutions are not only improving loan approval processes but also enabling more nuanced risk-based pricing and privacy-preserving credit assessments.

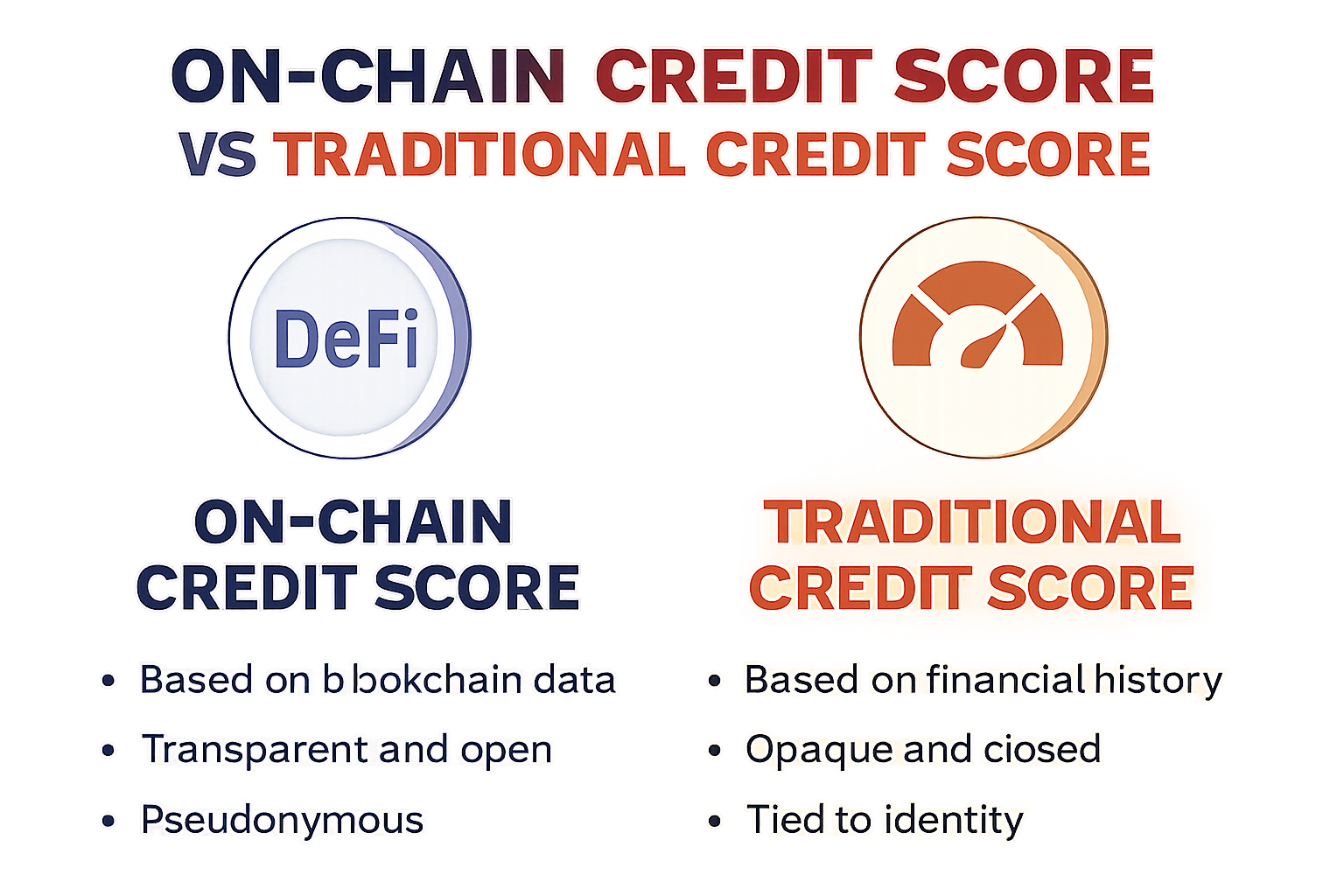

Transparency and interoperability are central themes in the current wave of on-chain credit innovation. Unlike opaque, proprietary algorithms in traditional finance, decentralized credit scoring protocols often publish their methodologies and allow open auditing of both data sources and scoring logic. This fosters a higher degree of user confidence and reduces the risk of systemic bias or hidden discrimination. Importantly, composability in DeFi means that a user’s on-chain credit reputation can be portable across multiple platforms, enabling a single score to unlock opportunities throughout the ecosystem.

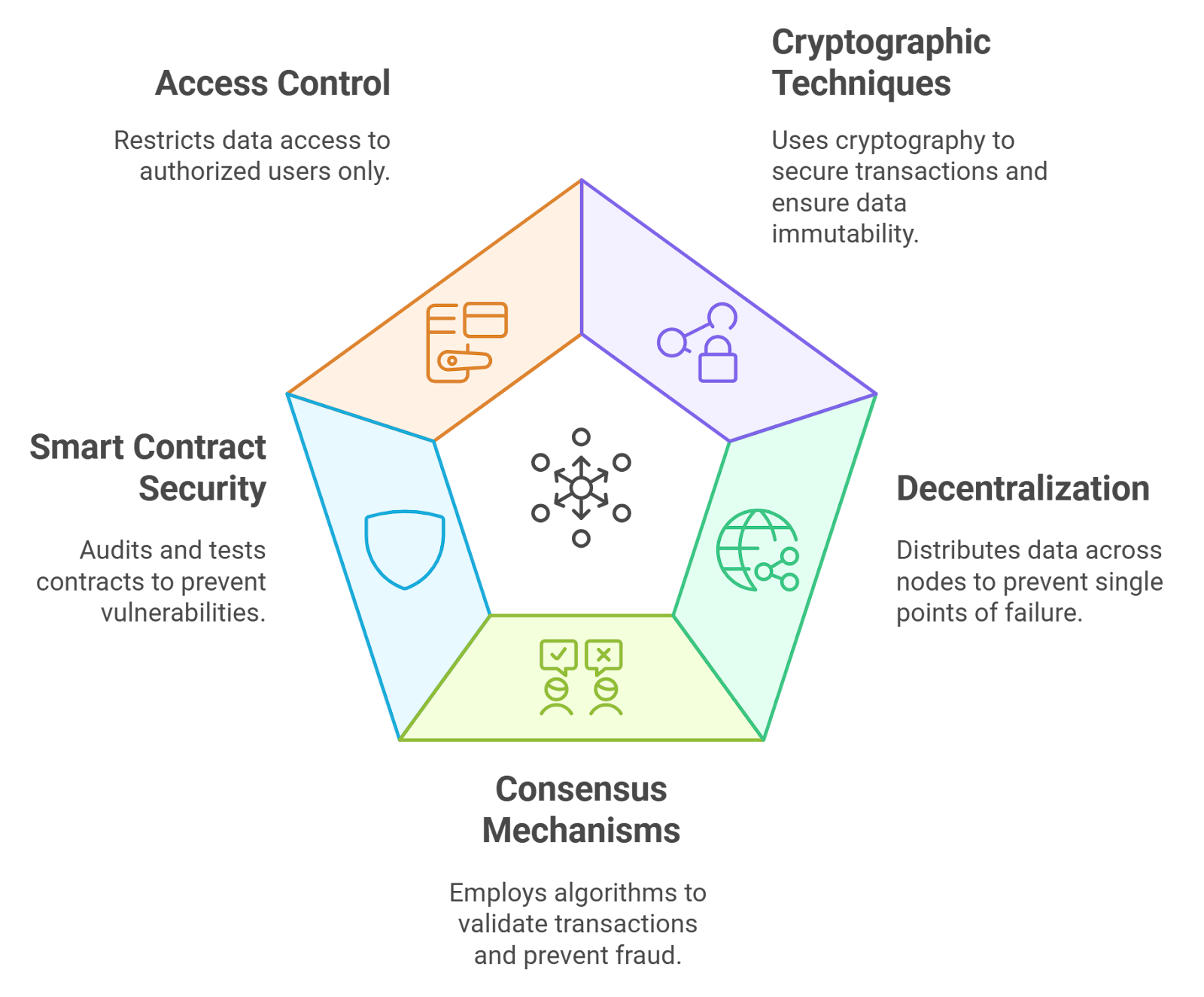

The push for standardized, privacy-preserving credit assessment is also gaining momentum. Zero-knowledge proofs and decentralized identifiers (DIDs) are being integrated to ensure that sensitive financial data remains private, even as it is verified and used for lending decisions. These cryptographic techniques allow users to prove their creditworthiness without exposing granular transaction histories, striking a balance between transparency and privacy that is nearly impossible in traditional systems.

Challenges and the Road Ahead

Despite rapid progress, decentralized credit scoring faces several hurdles. Data fragmentation remains a challenge, as user activity is often spread across multiple blockchains and protocols. Efforts to unify this data, such as cross-chain analytics and multi-protocol integrations, are ongoing, but true interoperability is still a work in progress. Additionally, while on-chain scores are resistant to manipulation, the risk of Sybil attacks (where one user creates multiple wallets to game the system) persists. Advanced identity solutions and behavioral analytics are emerging to address this, but widespread adoption is still needed.

Another key consideration is regulatory clarity. As real-world credit data flows onto blockchains and DeFi platforms begin to offer undercollateralized loans at scale, questions around compliance, data privacy, and consumer protection will grow more pressing. Proactive engagement with regulators and transparent governance processes will be critical for the long-term sustainability of decentralized credit bureaus.

Key Challenges Facing Decentralized Credit Scoring Adoption

-

Data Privacy and User Consent: Decentralized credit scoring platforms, such as ArthaNet and Spectral, require access to sensitive on-chain and sometimes off-chain data. Ensuring robust privacy protections and obtaining clear user consent remain major hurdles for widespread adoption.

-

Limited On-Chain Data Coverage: Many DeFi users have limited transaction histories or fragmented activity across multiple blockchains, making it difficult for platforms like Spectral and Credora to generate comprehensive and accurate credit scores.

-

Integration of Off-Chain Credit Data: Bridging traditional credit information with DeFi, as seen in TransUnion‘s and Untangled Finance‘s initiatives, faces technical and regulatory challenges, including data standardization and compliance with privacy laws.

-

Sybil Attacks and Identity Verification: Preventing users from creating multiple wallets to manipulate their credit scores is a persistent issue. Decentralized identity solutions are still evolving, making reliable identity verification a challenge for DeFi credit protocols.

-

Lack of Industry Standards and Interoperability: The absence of unified frameworks for decentralized credit scoring—such as the On-Chain Credit Risk Score (OCCR Score)—leads to inconsistent risk assessments and limits protocol interoperability across the DeFi ecosystem.

The Future of Trust and Lending in DeFi

The convergence of blockchain technology, advanced analytics, and privacy-preserving cryptography is setting the stage for a new era of trust in DeFi lending. As decentralized credit scoring matures, we can expect to see a dramatic expansion of DeFi loan approval options, ranging from microloans for emerging markets to institutional-grade credit lines for DAOs and enterprises. The result will be a more inclusive, efficient, and resilient financial system that leverages both on-chain data and traditional credit signals where appropriate.

For those building or participating in the next generation of DeFi protocols, now is the time to prioritize robust credit reputation frameworks. Not only do they enhance capital efficiency, but they also serve as the foundation for scalable, sustainable growth in decentralized finance. To explore more about how on-chain credit scores are transforming lending risks and benefits, visit this comprehensive guide.

Ultimately, the shift from collateral-based to reputation-based lending is not just a technical upgrade, it is a philosophical realignment that brings DeFi closer to its promise of open, fair, and accessible finance for all. As these systems continue to evolve, both users and protocols stand to benefit from a more nuanced understanding of risk and trust on the blockchain.