Decentralized finance (DeFi) has always promised open access to capital, but until recently, most lending protocols demanded borrowers lock up more collateral than they wished to borrow. This overcollateralization, while effective at minimizing risk, severely limits who can participate and how much liquidity can flow through crypto markets. Now, a new paradigm is emerging: on-chain credit scoring is enabling undercollateralized crypto lending, potentially unlocking trillions of dollars for the DeFi ecosystem.

Why Overcollateralization Holds DeFi Back

Protocols like Aave and Compound have popularized the model where users deposit assets as collateral and borrow a fraction of their value. While this reduces default risk, it also means that capital efficiency is low. Many users, especially those without substantial crypto holdings, are excluded from borrowing. The result? DeFi’s total accessible market remains a small fraction of global finance, and the system becomes less inclusive.

The core reason for this overcollateralization is simple: in a trustless environment, lenders need guarantees that loans will be repaid. Without a reliable way to assess borrower risk, the only protection is to demand more collateral than the loan itself.

Enter On-Chain Credit Scoring: Building DeFi Credit Reputation

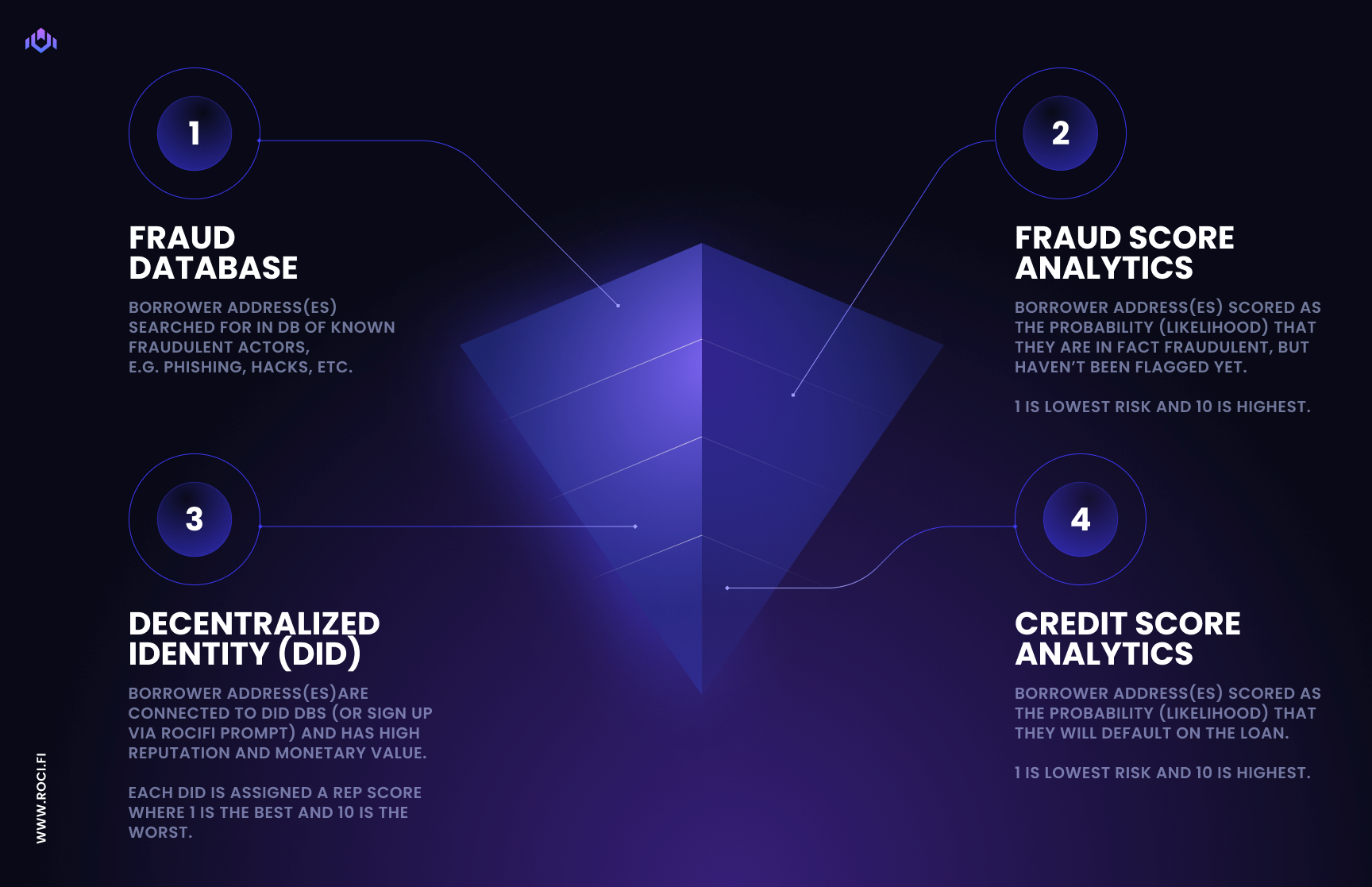

On-chain credit scoring transforms how risk is measured in decentralized lending. Instead of relying solely on collateral, protocols can now analyze a borrower’s blockchain activity, repayment history, wallet balances, participation in DAOs, and more, to generate a crypto credit score. This score acts as a decentralized reputation system, allowing protocols to gauge trustworthiness and offer undercollateralized or even unsecured loans.

Platforms like Cred Protocol, Credora, and Spectral Finance are at the forefront of this movement. For example, Credora’s partnership with More Protocol on Flow Blockchain allows users to borrow up to 200% of their collateral on MORE Markets by leveraging on-chain credit scores. Meanwhile, Spectral’s Multi-Asset Credit Risk Oracle (MACRO) score uses transaction data to assess risk and enable more flexible lending terms. These innovations are making it possible for DeFi users to build credit reputations that transcend individual protocols or chains.

How Blockchain Credit Assessment Works

So, what goes into a blockchain-based credit assessment? Unlike traditional credit bureaus that rely on opaque, off-chain data and centralized decision-making, on-chain credit scoring leverages transparent and verifiable blockchain activity. Key factors include:

Key Factors in On-Chain Credit Scoring for DeFi Lending

- On-Chain Repayment History: Consistent, timely repayment of previous DeFi loans is a major indicator of creditworthiness. Protocols like Cred Protocol and Spectral Finance analyze historical repayment data to assess risk.

- Wallet Asset Holdings: The value and diversity of assets held in a borrower's wallet, including stablecoins, blue-chip tokens, and NFTs, are evaluated to gauge financial stability and risk.

- Transaction Volume & Activity: High and regular transaction activity on-chain demonstrates engagement and reliability. Platforms like Credora factor in transaction frequency and size when generating credit scores.

- Past Liquidations & Defaults: Incidents where a borrower's positions were liquidated or loans defaulted negatively impact their on-chain credit score, as tracked by protocols such as Spectral Finance.

- Cross-Protocol Reputation: Credit scoring systems often aggregate data from multiple DeFi platforms (e.g., Aave, Compound, Maple) to build a holistic profile, rewarding positive behavior across the ecosystem.

- Identity Verification & KYC Status: Some undercollateralized lending protocols (like Maple and TrueFi) require KYC verification, which can enhance trust and improve credit scores for verified users.

- Smart Contract Interactions: Engagement with reputable DeFi protocols and the use of complex smart contracts can signal advanced user knowledge and responsible participation, contributing positively to credit assessments.

Protocols use advanced analytics and sometimes AI or machine learning to weigh these factors and assign a real-time score. This score can then be used by decentralized lending protocols to determine loan terms, reducing or even removing collateral requirements for users with strong credit reputations.

The Impact: More Capital, More Inclusion

By shifting from pure collateralization to DeFi credit reputation, the ecosystem stands to become far more accessible. Undercollateralized loans mean that users without large crypto portfolios, such as small business owners, freelancers, or those in emerging markets, can access capital for growth and innovation. According to industry analysis, this could bring trillions of dollars in new liquidity into DeFi as previously untapped markets gain access to decentralized capital.

Of course, this shift isn’t without its challenges. Protocols must balance the risks of default with the promise of greater inclusion and capital efficiency. But as on-chain data becomes richer and analytics more sophisticated, the vision of open, reputation-based lending is quickly becoming reality.

Undercollateralized crypto lending, powered by on-chain credit scoring, is not just a technical upgrade for DeFi, it’s a fundamental shift in how trust is established and financial opportunity is distributed. The data-driven approach of blockchain credit assessment means that anyone with a history of responsible on-chain activity can build a portable, privacy-preserving credit profile. This is particularly transformative for users previously locked out of traditional finance or those without substantial crypto assets to pledge as collateral.

Protocols Leading the Charge

Several decentralized lending protocols are already demonstrating what’s possible when blockchain credit assessment replaces rigid collateral requirements. Credora’s integration with More Protocol lets borrowers access up to 200% of their posted collateral on the Flow Blockchain, a dramatic increase in capital efficiency. Cred Protocol applies decentralized credit scoring to unlock lending for underserved communities, and Spectral’s MACRO score brings a new level of granularity to risk assessment by analyzing multi-asset wallet histories and behavioral patterns.

This expansion of DeFi’s credit layer is already attracting institutional interest and inspiring new models for decentralized lending. By quantifying trust on-chain, protocols are able to offer more competitive rates, longer loan durations, and tailored risk profiles, all without sacrificing security or transparency.

DeFi Protocols Using On-Chain Credit Scoring

- Credora partners with More Protocol to leverage on-chain credit scores on the Flow Blockchain, enabling users to access undercollateralized loans—borrowing up to 200% of their collateral on MORE Markets.

- Cred Protocol develops decentralized credit scores by analyzing users' on-chain activity, allowing borrowers to access undercollateralized loans and expanding DeFi lending to underserved communities.

- Spectral Finance provides a Multi-Asset Credit Risk Oracle (MACRO) score, which evaluates creditworthiness using on-chain transaction data and powers undercollateralized lending solutions across DeFi.

Risks, Challenges, and What’s Next

Despite these advances, undercollateralized lending still faces meaningful hurdles. Default risk remains a concern, especially as protocols stretch further from traditional collateral-backed models. There’s also the challenge of ensuring that on-chain credit scores are robust, resistant to manipulation, and sufficiently privacy-preserving. Many protocols are experimenting with hybrid models, combining on-chain data with off-chain verification or using permissioned pools for higher-risk borrowers.

Another challenge is interoperability. As users build their DeFi credit reputation across multiple chains and protocols, seamless portability of credit data becomes essential. Efforts like cross-chain credit oracles and standardized scoring frameworks are emerging to address this gap and create a more unified credit layer for Web3.

As DeFi matures, we’ll likely see a spectrum of lending products, from fully collateralized to fully reputation-based, giving users more choice and flexibility than ever before.

How On-Chain Credit Scores Impact the Future of Finance

The implications of on-chain credit scoring extend far beyond crypto native users. By making blockchain-based credit assessment accessible, DeFi can serve as a parallel financial system for the unbanked and underbanked worldwide. The ability to build and leverage a transparent, global credit score, without relying on centralized authorities, could fundamentally reshape lending, insurance, and even identity in the digital economy.

As these systems mature, expect to see new types of financial products emerge, dynamic credit lines, decentralized mortgages, or even portable business loans, all governed by transparent, programmable rules and real-time reputation signals.

Ultimately, the rise of undercollateralized crypto lending through on-chain credit scoring is about more than efficiency. It’s about trust, measured, earned, and proven on an open ledger. As protocols continue to innovate and users build their on-chain reputations, DeFi is poised to become not just more inclusive, but more resilient and dynamic than ever before.

No comments yet. Be the first to share your thoughts!