In 2024, decentralized finance (DeFi) lending platforms underwent a paradigm shift as on-chain credit scores became central to risk assessment, capital allocation, and borrower access. This transformation was driven by the need to move beyond rigid over-collateralization requirements and unlock trillions of dollars in latent capital for both borrowers and lenders. The integration of advanced blockchain credit assessments has made DeFi lending more efficient, transparent, and inclusive than ever before.

From Overcollateralization to Data-Driven Lending

Historically, DeFi lending protocols relied on overcollateralization to mitigate default risk. Borrowers needed to lock assets worth more than their loans - a model that restricted participation for users without substantial crypto holdings and limited overall capital efficiency. In contrast, on-chain credit scoring leverages granular blockchain data such as transaction histories, loan repayments, protocol interactions, and wallet behaviors. This enables the creation of a dynamic risk profile for each user or entity.

The result? Platforms can now offer undercollateralized or even unsecured loans to users with strong on-chain reputations. According to zkCredit and other industry sources, this approach not only brings fairer access for borrowers but also empowers lenders with improved risk controls and optimized capital allocation. The impact is reflected in hard data: by the end of 2024, open borrows across DeFi protocols reached $19.1 billion, nearly doubling centralized finance (CeFi) counterparts (source).

Pioneering Protocols: Real-World Adoption

The shift toward on-chain reputation-based lending is not theoretical - it’s already being implemented at scale by leading platforms:

Leading DeFi Platforms Using On-Chain Credit Scores (2024)

- Goldfinch pioneered undercollateralized lending by evaluating borrowers’ creditworthiness through a blend of on-chain and off-chain data, enabling access to capital for small businesses in emerging markets.

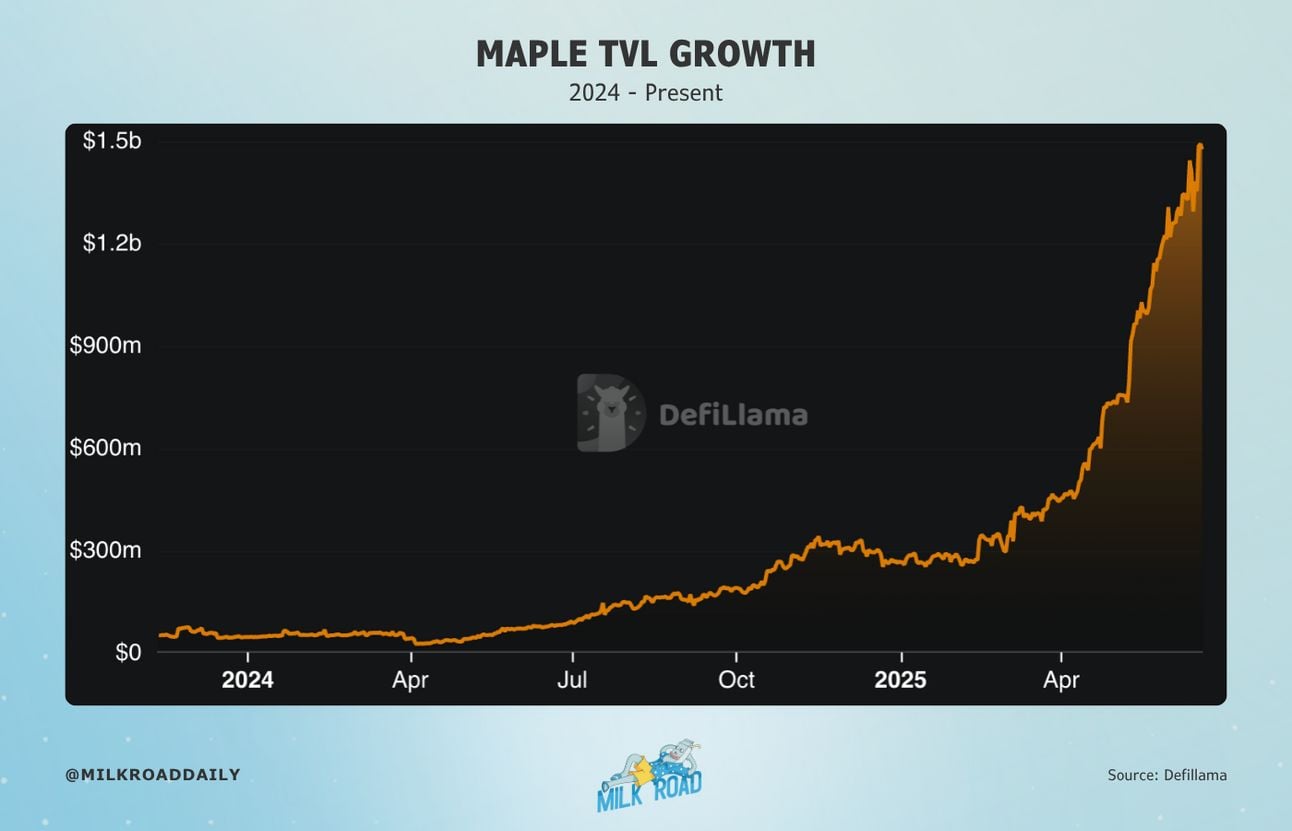

- Maple Finance utilizes a pool-delegate model where decentralized credit underwriters assess loan requests, combining off-chain due diligence with on-chain smart contract execution for efficient credit allocation.

- TrueFi integrates on-chain credit scoring and community governance to offer unsecured loans to trusted borrowers, leveraging a trust score system based on on-chain payment history and protocol interactions.

- Teller Finance bridges traditional and decentralized finance by incorporating zero-knowledge proof KYC and off-chain credit bureau data, enabling smart contract-based loans without collateral.

Goldfinch broke ground with undercollateralized loans using off-chain data for small businesses globally. Maple Finance introduced decentralized pool delegates who combine off-chain due diligence with smart contract-backed loans. TrueFi harnesses community-driven trust scores based on payment history and protocol engagement for unsecured lending opportunities. Meanwhile, Teller Finance bridges traditional credit bureaus with zero-knowledge proof KYC - all while maintaining privacy through cryptographic techniques.

This evolution is further accelerated by AI-powered analytics that continuously monitor wallet activity to generate real-time risk scores. These models dynamically adjust loan terms and interest rates based on borrower behavior - a leap forward from static legacy systems.

The Mechanics Behind On-Chain Credit Scores

On-chain credit scoring models, such as the On-Chain Credit Risk Score (OCCR), analyze public blockchain data points including:

- Lending/borrowing history: Repayment punctuality, defaults, rollovers.

- Diversity of protocol usage: Interaction with multiple reputable DeFi apps signals reliability.

- Wallet age and activity: Longer activity histories suggest established users versus new wallets created for malicious purposes.

- NFTs and asset holdings: Certain digital asset patterns can indicate financial stability or speculative risk.

- KYC/AML integrations: Optional layers using zero-knowledge proofs preserve privacy while enabling compliance where needed.

This multidimensional approach produces a transparent score that is portable across platforms yet resistant to manipulation or Sybil attacks. For a deeper dive into how these mechanisms work in practice, see our guide on on-chain credit scoring in DeFi lending.

The true power of on-chain credit scores lies in their ability to create a shared, verifiable reputation layer across the decentralized ecosystem. Unlike traditional credit bureaus, where data is siloed and often inaccessible, blockchain-based scoring models enable users to port their reputational capital between protocols seamlessly. This portability not only reduces onboarding friction for borrowers but also encourages responsible behavior, since positive actions are instantly reflected in one’s score across a range of DeFi platforms.

Protocols benefit by tapping into a richer risk dataset. For example, AI-driven analytics can detect patterns of wallet activity that may signal emerging risks or opportunities. Lenders can then recalibrate terms in real time, offering lower interest rates to proven borrowers or tightening requirements when risk indicators spike. This responsiveness is a direct result of transparent, on-chain analytics that are fundamentally more robust than off-chain alternatives.

Expanding Access and Reducing Systemic Risk

The impact extends beyond efficiency and transparency. By reducing the need for excessive collateral, on-chain credit scores open the door for underserved users, such as those lacking legacy financial histories, to participate meaningfully in global lending markets. As highlighted by recent industry analysis, this shift is already unlocking trillions in latent capital and driving user growth across emerging markets.

Moreover, these systems help mitigate systemic risk by enabling early detection of coordinated attacks or fraudulent borrowing patterns through cross-protocol data aggregation. The ability to trace wallet histories and verify behavioral consistency creates an environment where both lenders and borrowers can transact with greater trust, and where malicious actors find it much harder to game the system.

The Road Ahead: Challenges and Opportunities

Despite rapid progress, several challenges remain. Privacy concerns persist around sharing sensitive financial data, even in anonymized form. Zero-knowledge proofs (ZKPs) offer promising solutions by allowing users to prove aspects of their creditworthiness without revealing underlying details. Interoperability between scoring models is another priority; as standards mature, expect further convergence around open-source frameworks that facilitate cross-platform reputation portability.

- Data quality: Ensuring that input data is comprehensive and resistant to manipulation remains an ongoing battle.

- User education: Borrowers must understand how their actions affect scores, and how best to build strong on-chain reputations over time.

- Regulatory clarity: The evolving legal landscape will shape how KYC/AML integrations are implemented within decentralized protocols.

"On-chain credit scores are not just technical upgrades, they’re foundational for building trust at scale in permissionless finance. "

The momentum behind blockchain-based credit assessments is undeniable. As more protocols adopt these systems and as AI-powered analytics mature, expect continued growth in both lending volumes and user participation. For those seeking deeper insights into the mechanics and future implications of this trend, explore our resources on how on-chain credit scores are transforming DeFi lending platforms.

Key Benefits of On-Chain Credit Scoring for DeFi Protocols

- Enhanced Capital Efficiency: On-chain credit scores enable undercollateralized and uncollateralized lending, reducing the need for excessive collateral and allowing capital to be allocated more productively across DeFi platforms.

- Broader Financial Inclusion: By leveraging on-chain transaction histories and behaviors, DeFi protocols can offer loans to users who lack substantial crypto assets, expanding access to financial services for underbanked populations worldwide.

- Reduced Default Risk for Lenders: Data-driven risk assessments using on-chain credit scores allow lenders to better evaluate borrower trustworthiness, leading to lower default rates and improved portfolio performance.

- Increased Transparency and Trust: The use of publicly verifiable on-chain data for credit scoring increases transparency in lending decisions, fostering greater trust between borrowers and lenders.

- Dynamic Loan Terms and Interest Rates: Integration of AI-powered analytics with on-chain credit scores enables real-time adjustment of loan terms and interest rates based on up-to-date borrower risk profiles.

- Rapid Growth in Lending Activity: The adoption of on-chain credit scores contributed to DeFi open borrows reaching $19.1 billion by the end of 2024, nearly doubling the activity seen in centralized finance (CeFi) counterparts.

The rise of decentralized credit bureaus signals a new era for crypto lending, one defined by transparency, efficiency, and equitable access. In 2024’s competitive landscape, platforms leveraging robust on-chain analytics aren’t just managing risk, they’re actively shaping the future of open finance.

No comments yet. Be the first to share your thoughts!