Decentralized finance (DeFi) lending has entered a new era in 2025, powered by the rise of on-chain reputation scores. For years, DeFi was synonymous with over-collateralization: users had to lock up $1.50 or more in crypto to borrow $1, severely limiting capital efficiency and excluding millions from meaningful participation. That’s changing fast. Today, on-chain credit scores are unlocking under-collateralized DeFi lending, creating a decentralized credit bureau for Web3 and opening the doors to trillions in untapped liquidity.

Why Over-Collateralization Held DeFi Back

The original promise of DeFi lending protocols like Aave and Compound was open access to global liquidity pools. But without reliable ways to judge borrower risk, these platforms relied on brute-force security: demanding borrowers post more collateral than their loan’s value. This approach worked for whales and early adopters flush with crypto assets, yet it left out new users, small businesses, and emerging markets that lacked enough capital to participate.

Traditional finance uses credit bureaus to assess risk based on payment history and financial behavior. DeFi needed its own version, one that respected privacy, resisted manipulation, and ran entirely on transparent blockchain rails.

The Rise of On-Chain Reputation Scores

On-chain reputation systems are filling this gap by analyzing blockchain activity to gauge trustworthiness. Instead of relying on opaque off-chain data or personal identifiers, these protocols examine:

Key Factors in On-Chain Credit Scoring for DeFi Lending

- On-Chain Transaction History: Credit protocols analyze a user’s blockchain activity, including frequency, size, and diversity of transactions, to assess financial behavior and reliability.

- Loan Repayment Performance: Platforms like RociFi and Reputation DAO evaluate past DeFi loan repayments, late payments, and defaults to gauge borrower trustworthiness.

- Smart Contract Interactions: The number and type of smart contracts a user interacts with—such as lending, staking, or trading protocols—help indicate experience and risk profile.

- Fraud and Sybil Attack Risk: Advanced systems use AI models (like the zScore framework) to detect patterns of fraudulent or manipulative activity, reducing the risk of bad actors.

- Integration of Off-Chain Data: Some protocols, notably Reputation DAO, incorporate traditional credit scores, KYC, and social media activity to supplement on-chain data for a more holistic credit assessment.

- Reputation and Social Proof: Decentralized reputation systems aggregate peer reviews, endorsements, and community feedback to enhance credit scoring accuracy.

This data is synthesized into a dynamic score, the "on-chain credit score": that lenders can use to tailor loan terms and collateral requirements. Think of it as your Web3 financial passport: portable across protocols, privacy-preserving by design, and impossible to forge.

Platforms like RociFi have pioneered under-collateralized lending pools where your credit score determines how much collateral you need, or if you need any at all. Borrowers with high scores can access loans with minimal backing while those new or with riskier profiles face higher requirements or stricter terms. The result? Capital flows more freely to trustworthy users without exposing lenders to reckless default risk.

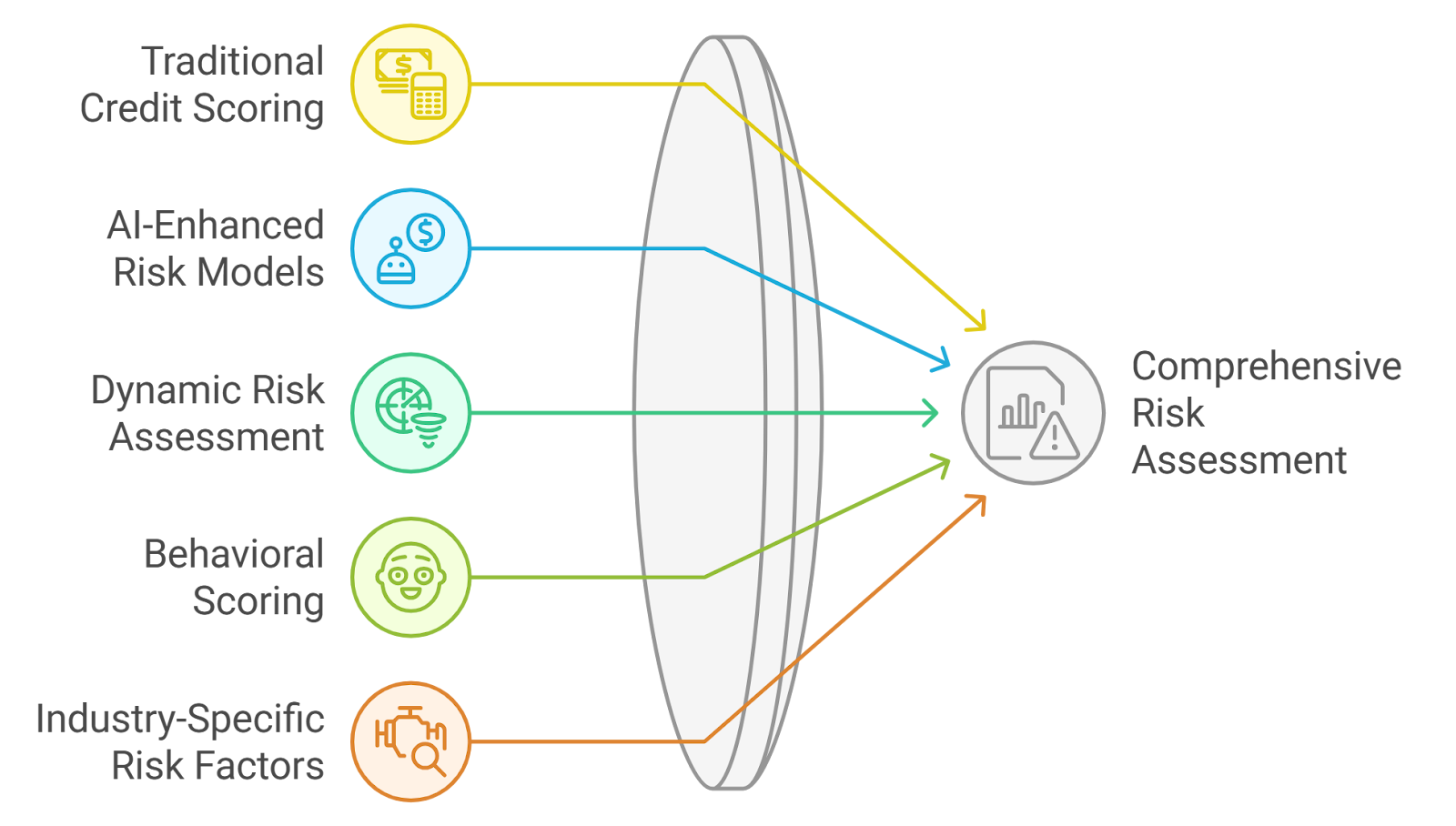

How AI and Hybrid Data Models Enhance Credit Protocols

The sophistication of DeFi reputation protocols has grown rapidly thanks to AI-powered analytics and hybrid data models. Reputation DAO blends on-chain behavior with select off-chain signals like traditional credit scores or even social media activity (opt-in), creating a holistic view of borrower reliability. Meanwhile, academic research such as the zScore framework leverages advanced machine learning models that spot patterns in repayment history across blockchains, predicting default risk with impressive accuracy.

This isn’t just theory; real-world results are compelling. Studies show a strong correlation between high zScores and responsible borrowing/repayment behaviors, a breakthrough for trustless finance. As these systems mature, they’re expected to bring trillions of dollars into DeFi by enabling safe under-collateralized loans at scale (more details here).

Key Benefits for Borrowers and Lenders

Top Advantages of Decentralized On-Chain Credit Scoring in 2025

- Enables Under-Collateralized Lending: On-chain credit scores empower DeFi platforms like RociFi to offer loans with reduced or no collateral, making borrowing more accessible to users who lack substantial crypto assets.

- Promotes Financial Inclusion: By assessing blockchain activity and integrating off-chain data, protocols such as Reputation DAO expand lending opportunities to users without traditional credit histories or significant collateral.

- Improves Capital Efficiency: On-chain reputation systems allow lenders to allocate capital more effectively, reducing the need for excessive collateral and unlocking greater lending volume across DeFi protocols.

- Enhances Transparency and Trust: Blockchain-based credit scoring leverages transparent, verifiable data, enabling lenders and borrowers to trust the integrity of the scoring process and loan terms.

- Reduces Default Risk with Data-Driven Insights: Advanced frameworks like zScore use AI to analyze on-chain behavior, providing accurate risk assessments and helping lenders mitigate potential defaults.

- Supports Multi-Source Credit Assessment: Integrating both on-chain and off-chain data (e.g., social media, traditional credit scores) allows for more comprehensive borrower evaluations, as seen with platforms like Reputation DAO.

The integration of decentralized identity verification, AI-driven analytics, and transparent scoring is creating a fairer playing field for everyone, from microloans in emerging markets to institutional-grade liquidity provision.

Borrowers are no longer defined solely by their asset holdings but by their proven on-chain behavior. This shift is particularly impactful for users in regions with limited access to traditional credit infrastructure. Microloans in DeFi, previously unthinkable due to high collateral demands, are now a reality, enabling entrepreneurs and everyday users to leverage blockchain-based capital for real-world needs.

For lenders, these advances mean better risk management and more diversified portfolios. By tapping into a transparent, immutable record of borrower reputation, protocols can dynamically adjust loan terms, interest rates, and even access tiers. This flexibility not only reduces default rates but also increases the overall yield for liquidity providers willing to serve a broader array of borrowers.

Decentralized Credit Bureaus: The Web3 Alternative

The emergence of decentralized credit bureaus, platforms that aggregate and standardize on-chain reputation data, is accelerating adoption across the DeFi ecosystem. Instead of relying on centralized gatekeepers or black-box algorithms, these bureaus use open-source scoring frameworks (like idOS credit scoring or zScore) to ensure fairness and composability across protocols.

As more lending platforms integrate these scores, we’re seeing the rise of interoperable DeFi identity: your reputation follows you across apps and chains, unlocking new financial opportunities without sacrificing privacy. For developers and DAO treasuries, this composability means they can plug into robust credit risk assessments without building complex systems from scratch.

This trend is especially visible as new entrants like Wildcat Labs experiment with innovative under-collateralized models, demonstrating that trust can be algorithmically earned rather than inherited from legacy institutions.

Challenges Ahead: Privacy, Sybil Resistance and Global Standards

Despite rapid progress, several hurdles remain. Sybil resistance: the ability to prevent one user from creating multiple identities to game the system, is a critical challenge for on-chain reputation protocols. Privacy is another major concern; while blockchain transparency enables accountability, it also raises questions about data exposure and user consent.

Standardization will be key as adoption grows. Without shared frameworks for scoring and identity verification, fragmentation could limit composability between DeFi protocols. Industry initiatives are underway to address these issues through zero-knowledge proofs (for privacy-preserving verification), decentralized identifiers (DIDs), and open-source governance models.

Looking Forward: The Future of Under-Collateralized DeFi Lending

The next wave of growth will likely come from further integration between on-chain reputation systems and real-world assets, blurring the line between crypto-native finance and traditional markets. As these decentralized credit bureaus mature, expect to see:

Key Trends Shaping Under-Collateralized DeFi Lending in 2025

- AI-Driven On-Chain Credit Scoring: Protocols like RociFi and zScore are leveraging advanced AI to analyze borrowers’ on-chain activity, improving risk assessment and enabling more accurate, dynamic credit scores.

- Integration of Off-Chain and On-Chain Data: Reputation DAO and similar platforms combine traditional credit information and social signals with blockchain behavior, creating comprehensive reputation profiles for under-collateralized lending.

- Expansion of Under-Collateralized Lending Pools: Platforms such as RociFi have launched lending pools where users with strong on-chain reputations can access loans with reduced or no collateral, boosting capital efficiency and financial inclusion.

- Decentralized and Transparent Credit Evaluation: On-chain credit scoring frameworks like zScore provide open, verifiable measures of creditworthiness, reducing reliance on centralized institutions and promoting trust in DeFi lending.

- Broader Financial Access and Inclusion: By utilizing on-chain reputation scores, DeFi platforms are reaching users without substantial crypto holdings, expanding lending opportunities to a wider global audience.

The vision is clear: a global financial system where access is based on transparent merit rather than arbitrary barriers or legacy privilege. For those ready to dive deeper into how these systems work under the hood, and what’s coming next, check out this guide or explore real-world case studies here.

As 2025 unfolds, on-chain credit scores aren’t just powering under-collateralized DeFi lending, they’re redefining trust itself for the decentralized age.

No comments yet. Be the first to share your thoughts!