Decentralized finance (DeFi) has long promised to democratize access to financial services, but until recently, its lending markets remained hampered by a fundamental limitation: the lack of reliable credit assessment. Overcollateralization was the norm, excluding millions who could not lock up significant crypto assets. The emergence of on-chain credit scores is rewriting these rules, offering a new paradigm for risk management and borrower inclusion in DeFi lending.

From Pseudonymity to Reputation: How On-Chain Credit Scores Work

Traditional credit scoring relies on centralized data silos and opaque algorithms. In contrast, on-chain credit scores leverage publicly available blockchain data, wallet transaction histories, protocol interactions, repayment behavior, to create transparent and auditable measures of trustworthiness. This decentralized approach means that users control their own reputational footprint and can selectively share their score with specific protocols or lenders.

The technical innovation here is profound. By analyzing patterns such as timely loan repayments, responsible asset management, and participation in governance or staking activities, these systems build a holistic profile without ever requiring real-world identity verification. As highlighted in recent research (see more), probabilistic models like the On-Chain Credit Risk Score (OCCR) are now quantifying risk with increasing sophistication, enabling DeFi platforms to move beyond blunt collateral requirements toward more nuanced underwriting.

"The future of DeFi lending lies in trustless yet reputation-driven interactions where your on-chain actions, not your off-chain paperwork, open doors to capital. "

The Benefits: Efficiency, Inclusion, and Transparency

Key Benefits of On-Chain Credit Scoring in DeFi

- Financial Inclusion: On-chain credit scores enable access to lending for users without traditional credit histories, expanding financial services to the unbanked and underbanked worldwide.

- Transparency and Verifiability: All credit assessments are performed on public blockchains, allowing users and lenders to verify how scores are calculated and ensuring assessment criteria remain consistent and auditable.

- User Control and Data Ownership: Individuals retain ownership of their on-chain financial data and can selectively share their credit reputation with specific DeFi protocols, enhancing privacy and user autonomy.

- Capital Efficiency: By enabling risk-based lending, on-chain credit scores allow borrowers with strong reputations to access loans with reduced or even zero collateral, making capital allocation more efficient for both users and lenders.

- Automated and Real-Time Risk Assessment: On-chain credit scoring leverages blockchain and AI to provide up-to-date risk profiles, allowing protocols to respond quickly to changes in borrower behavior and market conditions.

The impact of this shift is already visible across leading DeFi protocols:

- Financial Inclusion: Anyone with a blockchain wallet can build credit over time, even if they lack access to traditional banks or FICO scores. This levels the playing field for global users and underserved markets.

- Transparency: Assessment criteria are open-source and verifiable. Borrowers see exactly how their actions affect their eligibility for undercollateralized loans or better terms.

- User Control: Individuals own their reputational data and decide when, and to whom, to disclose it.

- Capital Efficiency: By reducing or eliminating collateral requirements for high-scoring borrowers, protocols can deploy liquidity more effectively while still managing risk.

This transformation is not just theoretical. Platforms like Aave now offer credit delegation features, while projects such as Goldfinch and Maple Finance enable undercollateralized loans for both crypto-native entities and real-world businesses, all powered by decentralized credit assessment frameworks.

Navigating Risks: Complexity, Manipulation and Regulation

No innovation comes without new risks. The pseudonymous nature of blockchain means that users can fragment their history across multiple wallets, a challenge for building comprehensive profiles. Blockchain’s immutability also means that outdated negative events may linger in a user’s record longer than warranted. And as these systems become integral to capital flows, incentives grow for bad actors to artificially inflate their scores through sybil attacks or wash trading.

Add regulatory uncertainty into the mix, since decentralized credit scoring doesn’t map neatly onto existing compliance frameworks, and it’s clear that robust risk management remains essential. AI-driven analytics are helping detect suspicious behaviors in real time, but ongoing refinement of methodologies will be key as both user activity and attacker sophistication evolve.

Pioneering Use Cases Across the Ecosystem

The practical applications are diverse:

- Aave's Credit Delegation: Users can delegate borrowing power based on established trust networks, enabling uncollateralized loans within defined boundaries.

- Goldfinch: Bridges crypto liquidity providers with vetted off-chain borrowers through hybrid reputation models.

- Maple Finance and TrueFi: Pool delegates and governance voters combine off-chain due diligence with on-chain transparency to offer unsecured loans to trusted entities.

This wave of innovation is only accelerating as platforms compete to attract both borrowers seeking flexibility and lenders seeking risk-adjusted yields based on transparent metrics rather than guesswork or brute-force collateralization. For a deeper dive into how these systems enable undercollateralized crypto loans, check out this resource: How On-Chain Risk Scores Enable Under-Collateralized Crypto Loans.

As DeFi lending platforms mature, the integration of on-chain credit scores is laying the groundwork for a more resilient and accessible financial ecosystem. It’s not just about removing barriers for borrowers - it’s about creating a robust feedback loop where positive on-chain behavior directly translates to better borrowing terms, and where risk is managed through open, auditable data rather than closed-door decisions.

Looking Ahead: The Evolution of DeFi Lending Risk Management

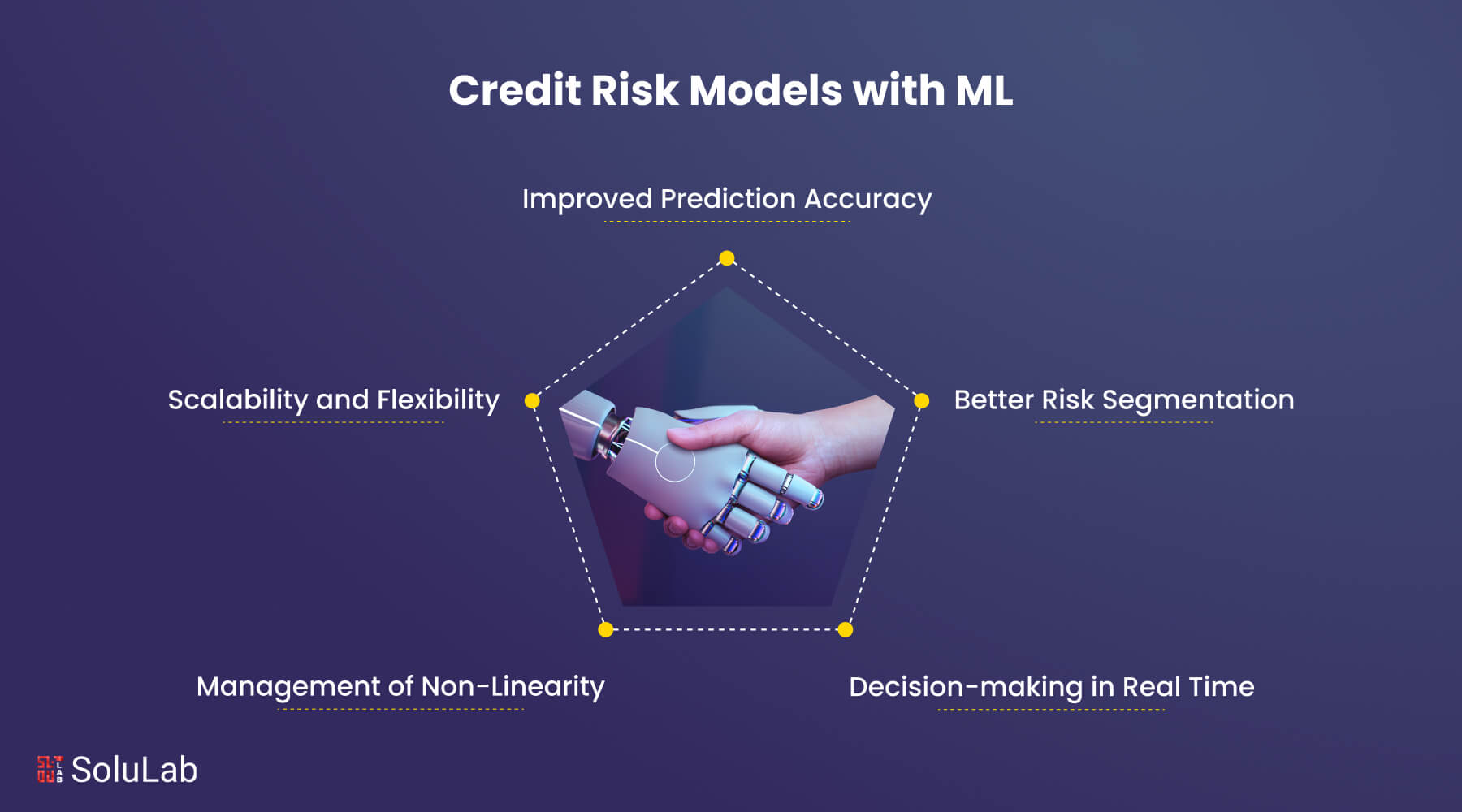

The next generation of DeFi credit platforms is already pushing boundaries by combining AI-powered analytics with on-chain transparency. These systems continuously monitor wallet activity, protocol participation, and repayment patterns to update risk assessments in real time. As highlighted by recent industry research, protocols are incorporating machine learning not only to detect fraud or sybil attacks but also to dynamically adjust credit limits and interest rates based on evolving user profiles.

For lenders, this means more granular control over portfolio risk exposure. For borrowers, it signals an era where reputation can be built and leveraged entirely within the crypto economy. This shift is especially transformative for users in emerging markets or those excluded from legacy finance - a trend that’s likely to accelerate as more protocols adopt decentralized credit assessment frameworks.

Key Challenges Hindering On-Chain Credit Scoring in DeFi

- Technical Complexity & Fragmented Identities: The pseudonymous nature of blockchain allows users to operate multiple wallets, making it difficult to build holistic credit profiles and accurately assess risk.

- Data Permanence & Outdated Information: Blockchain's immutability ensures data integrity but prevents the removal of obsolete or misleading credit data, which can unfairly impact users' current scores.

- Manipulation & Gaming of Scores: As on-chain credit scores gain influence, users may attempt to artificially inflate their scores through deceptive on-chain activity, requiring constant algorithmic updates to maintain integrity.

- Adapting to Rapidly Evolving DeFi Ecosystem: The fast-paced innovation and diversity of DeFi protocols challenge credit scoring models to remain relevant and accurate, especially with limited historical data.

- Regulatory Uncertainty: On-chain credit scoring operates in a regulatory gray area, with unclear compliance requirements that could expose platforms and users to legal risks as global regulations evolve.

- User Privacy & Data Ownership Concerns: While on-chain systems enhance transparency, they may also expose sensitive financial behaviors, raising concerns about privacy and control over personal data.

Key Considerations for Adoption

Despite the momentum, several hurdles remain before on-chain credit scoring can reach its full potential:

- Data Fragmentation: The ability for users to split activity across multiple wallets complicates holistic risk assessment. Solutions may include incentivizing reputation consolidation or developing cross-wallet identity standards.

- Algorithmic Bias: Scoring models must be regularly audited to prevent unintentional bias or manipulation that could disadvantage certain user groups.

- Privacy vs Transparency: Balancing open assessment criteria with user privacy will require ongoing innovation in zero-knowledge proofs and selective disclosure tools.

- Regulatory Alignment: As regulatory scrutiny increases, protocols will need agile compliance strategies that respect both user autonomy and legal obligations.

The industry’s response has been proactive: leading platforms are conducting regular security audits, stress-testing algorithms against adversarial tactics, and engaging with regulators to shape best practices. Community governance also plays a growing role in refining protocol-level risk frameworks and ensuring fair access across geographies.

Opportunities Beyond Lending: Building Trust Across Web3

The implications of decentralized credit assessment extend well beyond lending. On-chain trust scores are already being used as gatekeepers for DAO membership, whitelisting participants in token sales, and unlocking premium features across Web3 services. As these reputational layers mature, they promise to reduce friction throughout the decentralized economy - enabling everything from peer-to-peer insurance pools to collaborative investment clubs based on verifiable track records rather than personal connections or off-chain paperwork.

This evolution supports a more meritocratic financial landscape where opportunity flows according to transparent criteria rather than arbitrary gatekeeping. The challenge ahead lies in scaling these systems responsibly while maintaining the core values of privacy, autonomy, and inclusivity that define DeFi’s ethos.

The rise of on-chain credit scores marks a pivotal step toward trustless yet reputation-driven finance - one where your digital actions speak louder than your traditional credentials ever could.

If you’re interested in how developers can integrate these systems into their protocols or want deeper insights into undercollateralized lending mechanics, see our guides at How On-Chain Risk Scores Enable Under-Collateralized Lending in DeFi.

No comments yet. Be the first to share your thoughts!