Decentralized finance (DeFi) has redefined lending and borrowing, but its greatest challenge remains: building trust without intermediaries. Traditional finance relies on centralized credit bureaus and opaque risk models, while DeFi must create transparency and safety in a permissionless environment. Enter the on-chain credit score: a blockchain-native solution that is rapidly transforming how trust and risk are managed across DeFi lending markets.

How On-Chain Credit Scores Transform DeFi Lending Risk

Historically, most DeFi lending protocols have mitigated borrower risk by demanding overcollateralization. Users must lock up assets worth more than their loan value, which protects lenders but also limits capital efficiency and excludes many would-be borrowers. This system is blunt, treating all wallets as equally risky regardless of their actual on-chain behavior.

On-chain credit scores turn this paradigm on its head. By analyzing a user’s transaction history, asset holdings, repayment records, and broader blockchain activity, these scores provide a nuanced assessment of default risk. Lenders can now differentiate between high- and low-risk borrowers, enabling under-collateralized or even unsecured loans for those with strong crypto credit profiles. The result: improved capital allocation efficiency for lenders and fairer access to credit for borrowers.

Decentralized Credit Bureaus: Platforms Leading the Charge

The emergence of decentralized credit bureaus is reshaping the landscape. Pioneering platforms like Credora, Creditlink, CreDA, and RociFi are harnessing blockchain data to deliver real-time risk scoring:

Top Platforms Offering On-Chain Credit Scoring in DeFi

-

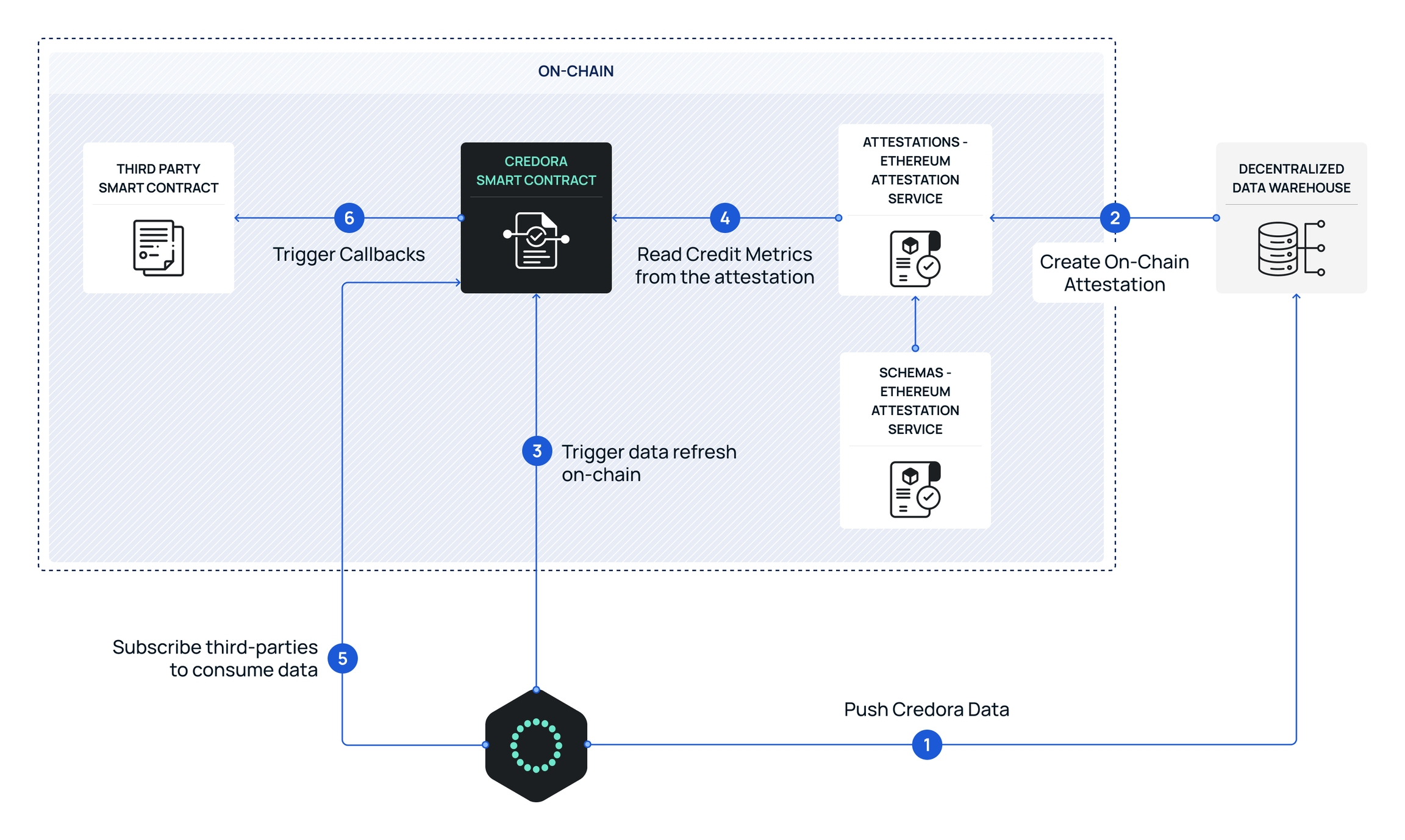

Credora: A leading platform bringing credit scores on-chain, Credora enhances transparency and efficiency in DeFi lending. Its credit assessments have facilitated over $1.5 billion in loans, and it partners with platforms like Clearpool to integrate programmatic credit scoring into lending markets.

-

Creditlink: Creditlink leverages AI and on-chain behavioral analysis to provide composable credit modules for DeFi and DAOs. Their credit scoring-as-a-service enables protocols to assess user creditworthiness for lending, protocol access, and identity verification.

-

CreDA (Credit DeFi Alliance): CreDA introduces personal credit scores to DeFi by analyzing users’ on-chain activity across multiple blockchains. Users can mint a Crypto Credit Score as a Credit NFT (cNFT), unlocking access to leveraged and low-collateral loans through partners like FilDA.

-

RociFi: RociFi offers Non-Fungible Credit Scores (NFCS), on-chain credentials that represent a user’s creditworthiness based on blockchain data such as balances and transaction history. These scores enable under-collateralized loans and broader financial access in DeFi.

– Credora: Integrates on-chain credit scores into programmatic lending markets, facilitating over $1.5 billion in loans through partners like Clearpool. – Creditlink: Uses AI to analyze wallet behavior across protocols, offering composable modules for DAOs and dApps. – CreDA: Issues Credit NFTs (cNFTs) representing a user’s cross-chain crypto credit score, unlocking leveraged or low-collateral loans. – RociFi: Introduces Non-Fungible Credit Scores (NFCS) as on-chain credentials that unlock under-collateralized borrowing opportunities.

This new wave of decentralized risk assessment is not just theoretical. According to recent research from zkCredit and arXiv (2025), these innovations could unlock trillions of dollars in untapped liquidity by making lending safer and more accessible for both sides of the market.

The Mechanics Behind Blockchain Credit Assessment

An effective blockchain credit assessment isn’t just about tallying up wallet balances. Advanced models ingest dozens of variables: frequency of repayments, participation in DAOs or governance votes, history with stablecoins versus volatile assets, even social graph analysis. Machine learning algorithms refine these models continuously as new data streams onto public ledgers.

This approach produces dynamic risk scores that update instantly with every transaction, a major leap over static reports from legacy bureaus. Lenders can set custom thresholds based on their own risk appetite or regulatory requirements. Borrowers benefit from transparency; they can see exactly which behaviors improve their standing over time.

The Benefits Ripple Across the Ecosystem

- Financial Inclusion: No need for traditional bank accounts or legacy FICO scores, anyone with an active crypto wallet can build a reputation.

- User-Controlled Data: Individuals maintain ownership over their financial history; privacy-preserving protocols let them choose what to share.

- Lender Confidence: Transparent metrics reduce counterparty risk while optimizing yields through smarter capital deployment.

- Ecosystem Growth: As trust grows, so does liquidity, a self-reinforcing cycle that benefits projects and users alike.

Yet, even as the infrastructure matures, the journey toward widespread adoption of on-chain credit scores in DeFi lending is not without obstacles. Technical hurdles, such as wallet fragmentation and the challenge of associating multiple addresses to a single user, remain significant. Moreover, the immutable nature of blockchain means that both positive and negative credit events persist indefinitely, raising questions about forgiveness and second chances in a decentralized world.

Despite these complexities, the potential upside is enormous. By leveraging transparent credit assessments powered by blockchain analytics, DeFi protocols can move beyond the era of one-size-fits-all overcollateralization. This evolution paves the way for more nuanced risk-based lending, where capital is allocated with precision and borrowers are rewarded for responsible on-chain behavior.

Real-World Impact: Lower Risk, Higher Trust

The integration of dynamic DeFi trust scores directly into lending protocols has already begun to reshape borrowing safety and capital efficiency. For example, platforms like Credora have facilitated over $1.5 billion in loans using on-chain credit data to inform their risk models. This approach minimizes default rates while expanding access to under-collateralized loans, an outcome nearly impossible under legacy systems.

Borrowers benefit from a fairer assessment process that recognizes their actual crypto activity rather than arbitrary external metrics. Lenders gain confidence through verifiable risk profiles that are constantly updated with each block mined. The result is a virtuous cycle: improved borrower outcomes drive increased liquidity, which in turn attracts more participants and further strengthens the ecosystem.

Practical Use Cases for On-Chain Credit Scores in DeFi Lending

-

Under-Collateralized and Collateral-Free Loans: Platforms like RociFi utilize on-chain credit scores to offer under-collateralized or even collateral-free loans, enabling borrowers with strong on-chain reputations to access capital without excessive collateral requirements.

-

Automated Risk Assessment for Lenders: Credora integrates on-chain credit scoring into lending protocols, providing lenders with transparent, real-time risk evaluations and facilitating more efficient capital allocation.

-

Composable Credit Modules for Protocols and DAOs: Creditlink offers credit scoring as a service, allowing DeFi protocols and DAOs to integrate credit checks for lending, protocol access, and identity verification.

-

Leveraged and Low-Collateral Loans via Credit NFTs: CreDA enables users to mint their on-chain credit score as a Credit NFT (cNFT), unlocking access to leveraged and low-collateral loans across partner platforms like FilDA.

-

Increased Financial Inclusion: By leveraging blockchain-based credit scores, DeFi platforms can provide fairer access to credit for users without traditional financial histories, expanding lending opportunities globally.

-

Transparent and Verifiable Credit Evaluation: On-chain credit scores ensure that all credit assessments are transparent and auditable, fostering trust between borrowers and lenders and minimizing information asymmetry.

What’s Next? Evolving Standards and User Empowerment

The future of decentralized credit bureaus will likely be defined by interoperability and user empowerment. As scoring methodologies mature, we can expect cross-chain reputation systems that aggregate data from multiple blockchains, offering a holistic view of user behavior regardless of where their assets reside. Privacy-preserving technologies will also play a pivotal role, ensuring that sensitive financial data remains under individual control while still enabling robust risk assessment.

For both lenders and borrowers navigating this new landscape, education will be crucial. Understanding how your crypto credit profile is calculated, and which behaviors influence your score, will become as important as managing private keys or understanding smart contract risks.

Yield is more than a number: In DeFi’s next chapter, trust itself becomes programmable, and risk becomes an opportunity for everyone willing to build their reputation on-chain.

If you’re interested in exploring how under-collateralized lending works with on-chain risk scores or want deeper insights into decentralized credit assessment frameworks, check out our detailed guides at Crypto Credit Scores.