Collateral requirements have long been the gatekeepers of decentralized finance. In traditional DeFi lending, users often have to lock up more value than they borrow, sidelining countless would-be borrowers and stunting capital efficiency. But a new wave of on-chain reputation systems is rewriting the rules, enabling DeFi lending without collateral and opening the door to trillions in new liquidity.

The Shift From Collateral to Reputation-Based Lending

Why does this matter now? As of September 24,2025, capital is flowing into DeFi at unprecedented rates. Ethereum (ETH) is trading at $4,172.97, with Aave (AAVE) at $279.58 and Compound (COMP) at $41.94. These platforms are evolving rapidly, but over-collateralization remains a bottleneck for broader adoption.

Creditlink and other innovators are introducing decentralized identity (DID) and verifiable credentials that allow lenders to dynamically assess risk based on blockchain behavior - not just wallet balances. Suddenly, your reputation matters more than your collateral.

How On-Chain Reputation Scores Work

On-chain credit scores analyze public blockchain data: transaction history, loan repayments, DApp interactions, and even social attestations. This transparent record forms a living credit profile that protocols can tap into for real-time risk assessments.

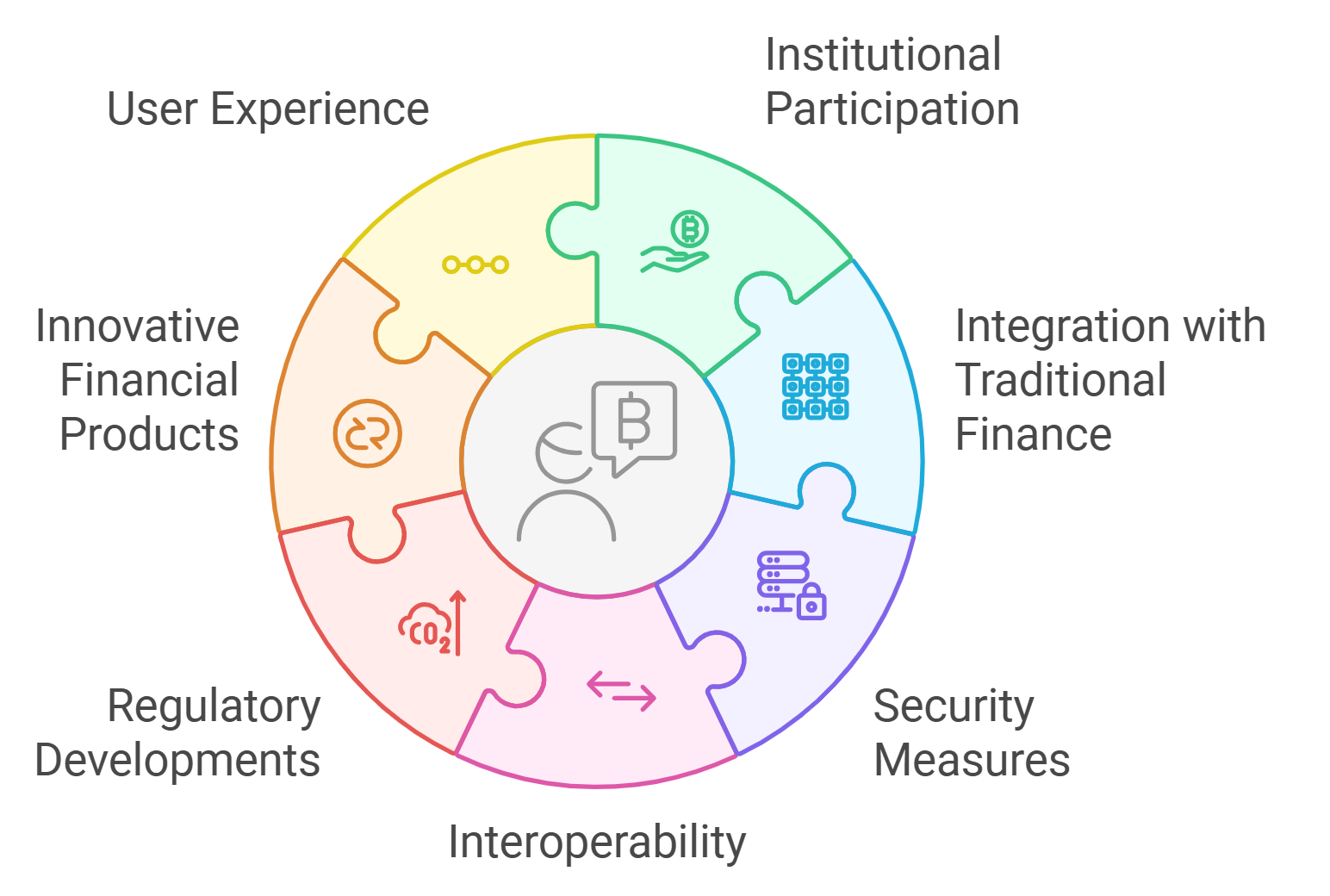

Key Factors Shaping On-Chain Reputation Scores in DeFi Lending

- Decentralized Identity (DID) and Verifiable Credentials: Solutions like Creditlink utilize DID systems to verify user identities and aggregate on-chain behavior, generating dynamic credit scores (e.g., 300 to 1000). Higher scores can unlock reduced or zero collateral requirements.

- Integration of Off-Chain Data: Protocols such as Reputation DAO incorporate traditional credit information, KYC, and AML data to provide a holistic view of a borrower's reliability, enabling undercollateralized lending.

- Soulbound Tokens (SBTs): Inspired by non-transferable game items, SBTs are permanently tied to a user's blockchain address. Accumulating SBTs—representing credit scores or trusted attestations—enhances credibility for collateral-free lending.

- Social and Community Attestations: Some DeFi protocols leverage endorsements from reputable entities or community members, adding a layer of trust to reputation scores and incentivizing responsible financial behavior.

The result? Users with strong on-chain reputations can access loans with little or no collateral - a game-changer for those without deep crypto pockets.

The Tech Behind Decentralized Credit Assessment

This isn't just about tracking wallet activity. Modern protocols are blending on-chain analytics with off-chain data like AML/KYC checks or even traditional credit scores. For example, Reputation DAO integrates external data streams for holistic borrower profiles while maintaining privacy through cryptographic proofs.

Soulbound tokens (SBTs), inspired by non-transferable items in gaming, are also gaining steam as digital badges of trustworthiness tied directly to your address - think permanent proof of good behavior or endorsements from respected entities. Accumulating SBTs can unlock new tiers of borrowing power in emerging protocols.

The Benefits: Inclusion, Efficiency, and Behavior Incentives

The implications ripple across the entire crypto ecosystem:

- Enhanced financial inclusion: No more exclusion based solely on asset holdings; anyone with verifiable good behavior can participate.

- Improved capital efficiency: Less over-collateralization frees up liquidity for active deployment across DeFi markets.

- Sustainable risk management: Borrowers are incentivized to maintain stellar reputations or risk losing future access - aligning interests between lenders and borrowers like never before.

This is just the start. As protocols refine their models and adoption grows, expect the line between traditional credit assessment and blockchain innovation to blur even further - all while keeping user privacy front and center through advanced cryptography.

Protocols like Reputation DAO are at the forefront, showing how decentralized credit assessments can safely bridge on-chain and off-chain worlds. The use of cryptographic proofs means users can prove their trustworthiness without surrendering sensitive personal data - a crucial evolution for privacy-conscious borrowers. This paradigm shift doesn’t just enable DeFi lending without collateral. It’s actively redefining what risk, trust, and opportunity look like in the decentralized economy.

Platforms are also experimenting with gamified incentives: think loyalty rewards, NFT badges for consistent repayments, or community-driven attestations that boost your blockchain credit scoring profile. These mechanisms make responsible borrowing not just prudent but profitable, further aligning user behavior with protocol health.

Real-Time Market Impact: Prices Reflect Growing Confidence

The numbers tell their own story. As of September 24,2025:

With Ethereum (ETH) holding steady at $4,172.97, Aave (AAVE) at $279.58, and Compound (COMP) at $41.94, investor confidence is surging around protocols that embrace reputation-based lending models. These price points underscore the market’s appetite for scalable solutions to DeFi’s collateral bottleneck.

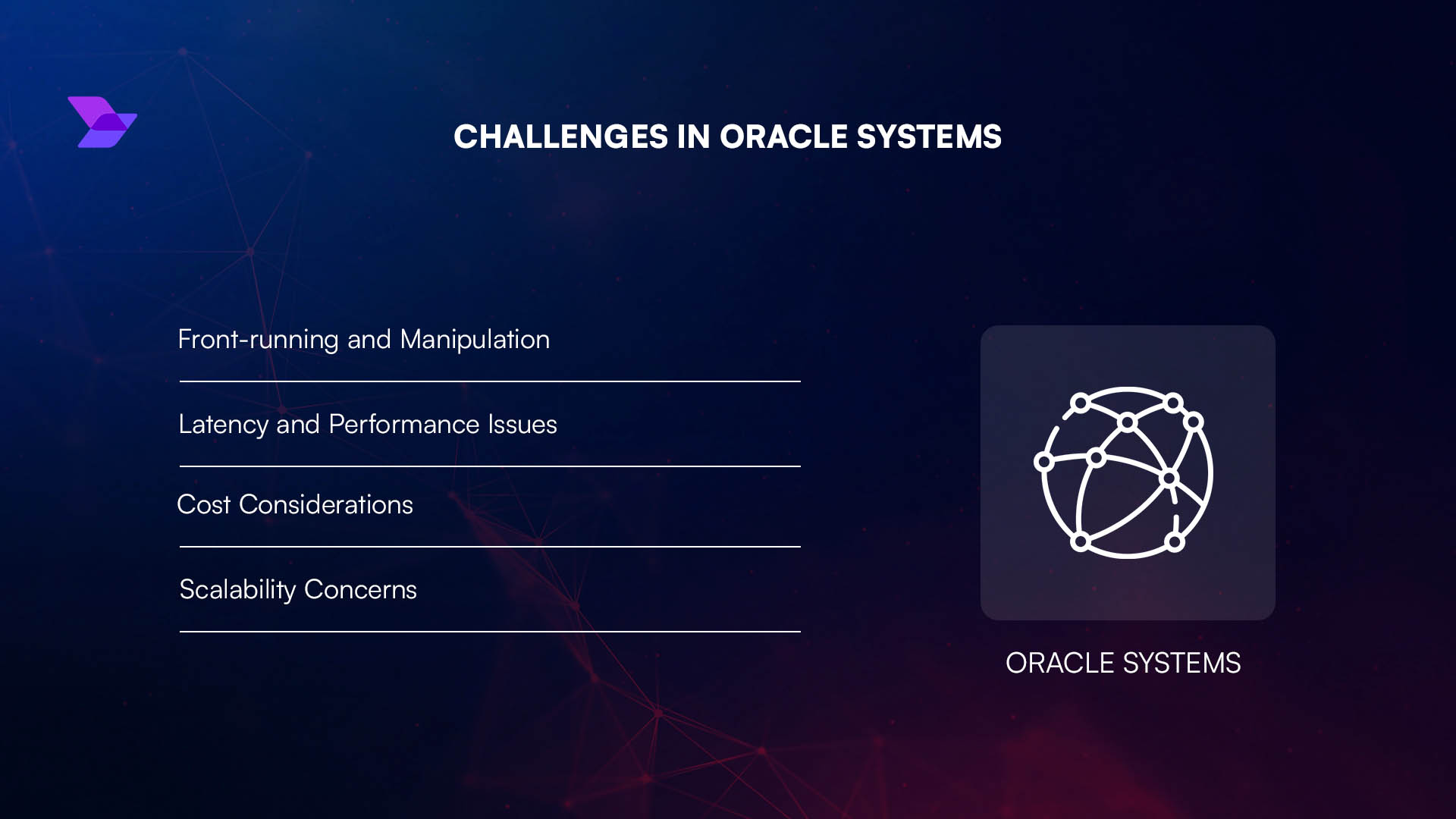

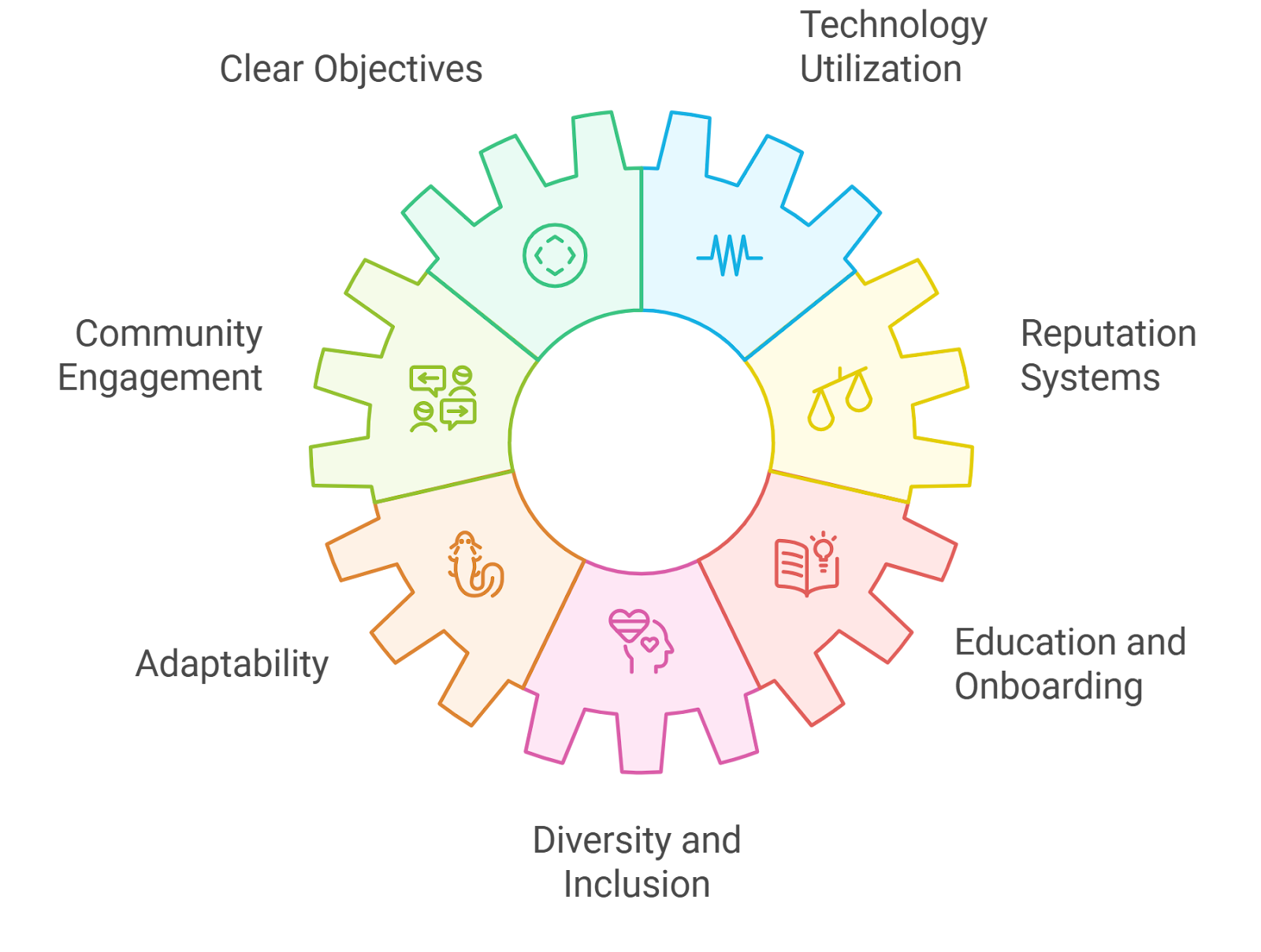

Challenges Ahead: Risks and Open Questions

No system is bulletproof - not even decentralized credit scoring. Sybil attacks (where one entity controls many pseudonymous accounts), manipulation of on-chain activity to game scores, and privacy trade-offs remain active areas of research and debate. Protocols are racing to implement robust identity frameworks and fraud detection tools to keep reputation-based lending both fair and resilient.

Key Challenges for On-Chain Reputation in DeFi

- Privacy and Data Security: Balancing transparency with user privacy is tough. Integrating off-chain data (like KYC/AML) risks exposing sensitive information, challenging DeFi’s ethos of anonymity.

- Sybil Attacks and Identity Fraud: Without robust decentralized identity (DID) solutions, malicious actors can create multiple wallets to manipulate reputation scores, undermining trust in lending protocols.

- Standardization and Interoperability: Diverse reputation models (e.g., Creditlink, Reputation DAO) lack unified standards, making it hard for scores to be recognized across different DeFi platforms.

- Integration of Off-Chain Data: Bridging traditional credit data with on-chain activity (as seen with Reputation DAO) is complex and may introduce regulatory and technical hurdles.

- Reputation Score Manipulation: Users may game on-chain metrics (like transaction history) to artificially boost their scores, threatening the accuracy of credit assessments.

- Adoption and Network Effects: For reputation systems to work, broad adoption is critical. Fragmented user bases and lack of incentives can slow network effects and limit effectiveness.

Another question looms large: How will regulators respond as real-world assets flow into these systems? The intersection of compliance, privacy, and programmable finance will shape the next wave of innovation - or friction - in this space.

The Road Ahead: Building Trust Without Borders

The future is bright for decentralized credit assessment. By merging transparent blockchain data with advanced analytics and privacy-preserving tech, protocols are finally unlocking the holy grail of crypto finance: trust without intermediaries or barriers.

If you’re a borrower ready to leverage your on-chain reputation or a lender seeking new risk models, now’s the time to pay attention. The race to onboard the next trillion dollars into DeFi isn’t just about liquidity - it’s about building a fairer financial system where your actions matter more than your assets.

Would you trust an on-chain reputation score more than a traditional credit check when lending or borrowing in DeFi?

On-chain reputation systems are transforming DeFi lending by enabling collateral-free or undercollateralized loans, using blockchain data to assess creditworthiness. With platforms now integrating both on-chain activity and off-chain data, would you feel more confident relying on these scores compared to traditional credit checks?

No comments yet. Be the first to share your thoughts!