Decentralized finance has long promised open access to capital, but for years, borrowing in DeFi meant locking up more assets than you received in return. This over-collateralization model, while effective at minimizing risk, has left trillions of dollars of potential liquidity untapped. Now, a new generation of on-chain credit scoring protocols is rewriting the rules by enabling unsecured DeFi lending: and the impact is already visible across the ecosystem.

Why Over-Collateralization Limits DeFi’s Potential

Traditional DeFi lending protocols like Aave and Compound have always required users to deposit more crypto than they borrow. This design protects lenders from default but restricts capital efficiency, especially for those without deep pockets. The result? Many would-be borrowers are locked out, and vast sums sit idle as collateral rather than fueling innovation or economic activity.

This inefficiency has become increasingly apparent as DeFi matures. The next logical evolution: using blockchain data to assess borrower risk, just as banks use credit scores in traditional finance. Enter the era of on-chain credit scores.

The Mechanics of On-Chain Credit Scoring

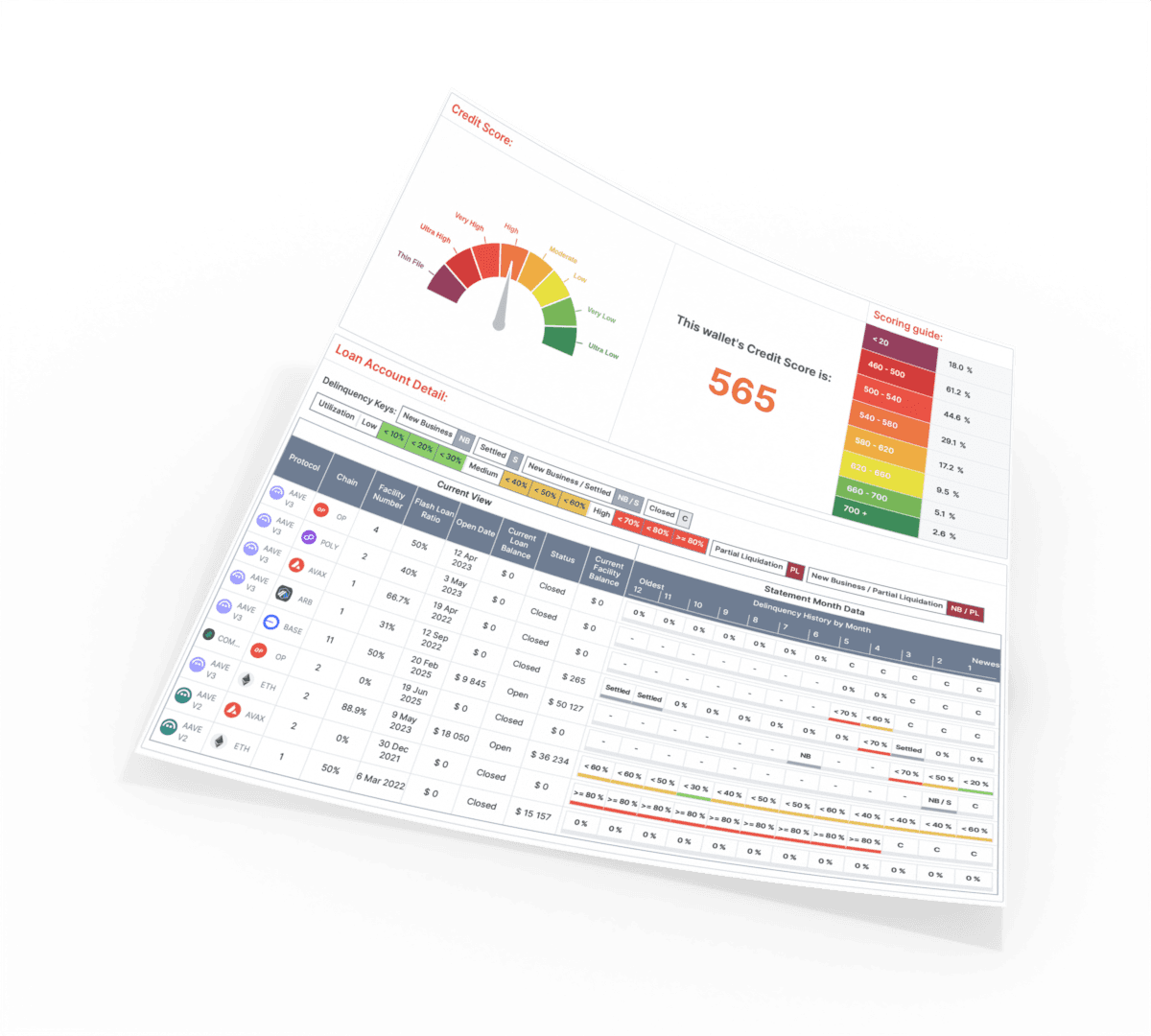

On-chain credit scoring systems analyze a user’s blockchain activity, transaction history, repayment records, protocol interactions, to build a data-rich picture of their financial reputation. Unlike legacy systems that rely on opaque data brokers or centralized bureaus, these decentralized models are transparent and privacy-preserving by design.

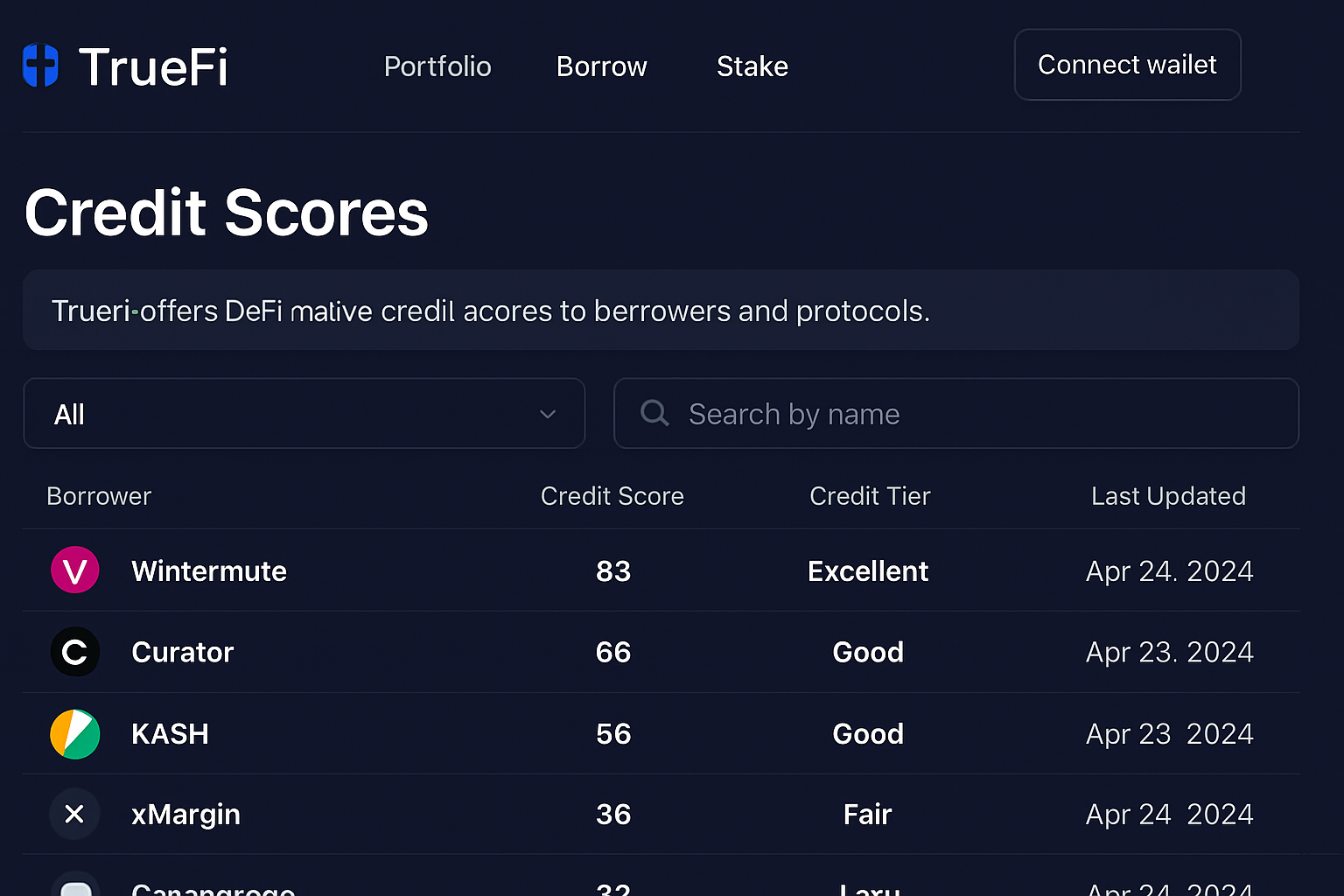

This shift is not just theoretical. Projects like TrueFi, Cred Protocol, and Creditlink are pioneering robust models that allow lenders to assess risk dynamically and offer loans with little or no collateral required.

Key Benefits of On-Chain Credit Scores in DeFi Lending

- Unlocking Unsecured and Under-Collateralized Loans: On-chain credit scores enable DeFi protocols like TrueFi and Cred Protocol to offer loans without requiring borrowers to lock up assets exceeding the loan value, making capital more accessible and efficient.

- Enhancing Capital Efficiency: By reducing or eliminating the need for over-collateralization, on-chain credit scoring systems free up user capital, allowing funds to be used more productively across DeFi markets.

- Promoting Financial Inclusion: Platforms such as Credora and Creditlink use on-chain activity to assess creditworthiness, enabling users with limited traditional assets to access lending opportunities based on their blockchain reputation.

- Encouraging Responsible On-Chain Behavior: Borrowers are incentivized to maintain good financial practices—such as timely repayments and prudent borrowing—since these behaviors directly impact their on-chain credit score and future borrowing terms.

- Increasing Transparency and Trust: On-chain credit scores, as implemented by Credora, provide transparent and verifiable borrower histories, reducing information asymmetry and helping lenders make informed decisions.

- Bridging Traditional and Decentralized Finance: Integrations like TransUnion's on-chain credit data allow DeFi platforms to leverage both real-world and blockchain-based credit information, resulting in more comprehensive risk assessments.

The result? Borrowers with strong blockchain reputations can access capital more efficiently while lenders gain new tools for DeFi risk assessment. Everyone wins, if the system works as intended.

Who’s Leading the Charge? Key Protocols Shaping the Market

The landscape is evolving quickly as both established players and ambitious startups compete to define how decentralized credit will work at scale:

- TrueFi: Blending on-chain and off-chain data to originate over $100 million in unsecured loans without defaults so far (source). Their model proves that reputation-based lending can compete with traditional methods in terms of reliability.

- Cred Protocol: Pushing under-collateralized lending forward by quantifying individual wallet risk profiles using only blockchain data (source). Their decentralized scoring system is open to all, helping users build portable financial identities.

- Creditlink: Innovating with trustless, privacy-first scores ranging from 300-1000, dynamic numbers that directly influence collateral requirements (source). This approach lets borrowers unlock better terms by demonstrating responsible behavior on-chain.

- Credora: Bringing transparency to institutional lending markets by benchmarking on-chain scores against legacy ratings; over $1.5 billion in loans facilitated so far (source).

- TransUnion: Bridging Web2 and Web3 by making real-world credit scores available directly within blockchain applications (source). This hybrid approach offers a fuller picture of borrower trustworthiness.

The Broader Impact: Capital Efficiency Meets Financial Inclusion

The implications go beyond convenience; they strike at the core promise of decentralized finance itself. By decoupling borrowing power from asset holdings and linking it instead to blockchain reputation, these protocols are opening doors for users historically excluded from global capital markets.

This isn’t just about bigger loans or better rates, it’s about building a fairer system where your financial history is portable, transparent, and owned by you. As more protocols adopt these models, expect competition (and innovation) around privacy features, score portability across chains, and even cross-border lending opportunities.

Real-World Ways On-Chain Credit Scores Boost Financial Inclusion

- TrueFi’s Blockchain Credit Scoring Model enables users worldwide to access unsecured loans based on their on-chain reputation, rather than requiring traditional collateral. This opens up lending opportunities for individuals who lack substantial assets but demonstrate responsible blockchain activity.

- Cred Protocol’s Decentralized Credit Scores quantify lending risk using blockchain data, allowing under-collateralized borrowing. This approach helps users in emerging markets, who may have limited access to conventional credit, participate in DeFi lending and borrowing.

- Creditlink’s Trustless, Privacy-Preserving Scores assign dynamic credit ratings using decentralized identity and verifiable credentials. This system reduces collateral requirements for trustworthy users, making DeFi loans more accessible to those with strong on-chain reputations but limited upfront capital.

- Credora’s On-Chain Credit Scores bring transparency and accessibility to lending by benchmarking on-chain credit assessments against traditional ratings. This has enabled over $1.5 billion in loans, demonstrating the scalability and inclusion potential of on-chain scoring systems.

- TransUnion’s Integration of Real-World Credit Scores with DeFi platforms allows users to leverage their traditional credit histories when applying for blockchain-based loans. This bridges the gap for those with strong off-chain reputations but limited crypto collateral, expanding DeFi access to a broader population.

Yet, the shift to unsecured DeFi lending isn’t without its growing pains. Risk management is paramount. Protocols are racing to refine their credit models, implement dynamic interest rates based on real-time scores, and develop circuit breakers for systemic shocks. The stakes are high: a poorly calibrated system could invite cascading defaults or open the door to sophisticated attacks.

That’s why many leaders in the space are doubling down on transparency and open-source analytics. On-chain credit scoring means anyone can audit the logic behind a protocol’s risk assessment. This radical openness stands in sharp contrast to legacy credit bureaus, which operate as black boxes.

What’s Next? The Road to Trillions in On-Chain Credit

The momentum is undeniable. According to Onchain, the integration of on-chain credit scores could unlock trillions of dollars in new liquidity for DeFi markets, capital that’s currently sidelined by collateral requirements or lack of access to traditional banking rails.

Protocols like 3Jane and Goldfinch are experimenting with novel risk tranching, insurance pools, and decentralized dispute resolution mechanisms. Meanwhile, pilots like Mercy Corps’ micro-lending initiative are proving that even informal entrepreneurs and underbanked users can tap global liquidity if they build a blockchain reputation. The flywheel effect is real: more data leads to better scores, which attract more lenders, which further expands access.

As competition heats up, expect decentralized credit protocols to push innovation even further, think reputation NFTs for wallets, cross-protocol score portability, or AI-driven fraud detection powered by open blockchain data.

Checklist: What Lenders and Borrowers Should Watch For

If you’re considering diving into unsecured DeFi lending as a lender or borrower, keep these essentials top of mind:

- Score Transparency: Can you independently verify how your score is calculated?

- Privacy Controls: Does the protocol safeguard your wallet data?

- Lending Terms: Are rates and limits clearly linked to your on-chain activity?

- Dispute Resolution: Is there a fair process if something goes wrong?

- Ecosystem Support: How widely is this scoring model accepted across protocols?

Why On-Chain Credit Scores Are Here To Stay

The old rules of finance were built around exclusion and opacity; DeFi has the chance to flip that script with transparent, programmable trust. As on-chain credit scores mature, integrating richer data sources and more nuanced risk metrics, they will become foundational infrastructure for both everyday users and institutional capital alike.

The next wave of growth will likely come from protocols that balance privacy with transparency, portability with security, and accessibility with robust risk controls. Whether you’re a crypto newcomer seeking your first loan or an established project looking for efficient capital allocation tools, understanding how these systems work will be crucial.

The bottom line? In decentralized finance, your knowledge, and your digital reputation, are now your best collateral.

No comments yet. Be the first to share your thoughts!