Decentralized finance is undergoing a seismic shift as on-chain credit scores redefine the mechanics of DeFi lending. For years, the lack of reliable blockchain credit assessment forced lending protocols to demand excessive collateral from borrowers, locking up capital and stifling growth. Now, by leveraging transparent on-chain data and advanced analytics, DeFi platforms are finally bridging the gap between trustless infrastructure and personalized financial services.

From Over-Collateralization to Data-Driven Lending

Historically, DeFi lending protocols operated under a simple but inefficient model: require users to over-collateralize loans, sometimes by 150% or more. This approach was necessary because there was no way to gauge a user’s trustworthiness without traditional credit bureaus. The result? Billions in idle assets sitting in smart contracts, and a system that excluded anyone unable or unwilling to lock up disproportionate collateral.

The emergence of on-chain credit scoring mechanisms has fundamentally altered this dynamic. By evaluating a user’s transaction history, wallet behavior, protocol participation, and even their performance across multiple blockchains, these systems generate decentralized risk profiles that can be instantly verified by smart contracts. According to Credora, integrating real-time credit scores on-chain enhances both transparency and capital efficiency for lenders and borrowers alike.

The Leading Protocols Powering On-Chain Credit Scores

Leading DeFi Projects in On-Chain Credit Scoring

- Credora integrates on-chain credit scores to enhance transparency and efficiency in DeFi lending. Its partnerships with platforms like Clearpool and Obligate advance on-chain credit markets and innovative lending solutions.

- Spectral uses its Multi-Asset Credit Risk Oracle (MACRO) to generate on-chain credit scores from blockchain transaction histories. These are tokenized as Creditworthiness NFTs (cwNFTs), enabling users to access improved borrowing rates across DeFi.

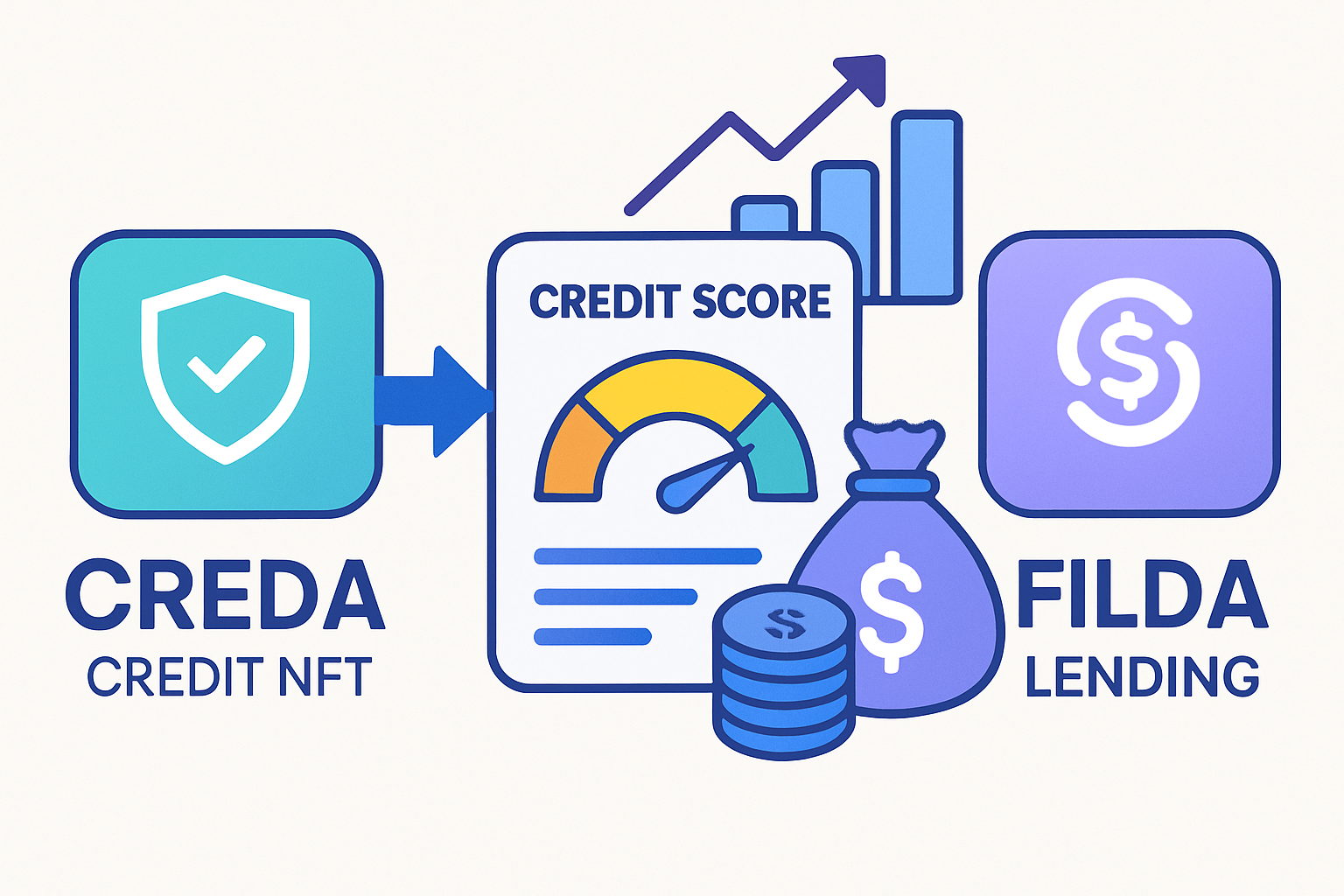

- CreDA (Credit DeFi Alliance) analyzes on-chain activities across multiple blockchains to provide decentralized credit ratings. Users can mint Crypto Credit Scores as Credit NFTs (cNFTs) and access leveraged, low-collateral loans through partners like FilDA.

- Reputation DAO bridges DeFi and traditional finance by leveraging real-world financial data and on-chain analytics. Its data flow engine assesses risk and enables more capital-efficient lending with reduced over-collateralization.

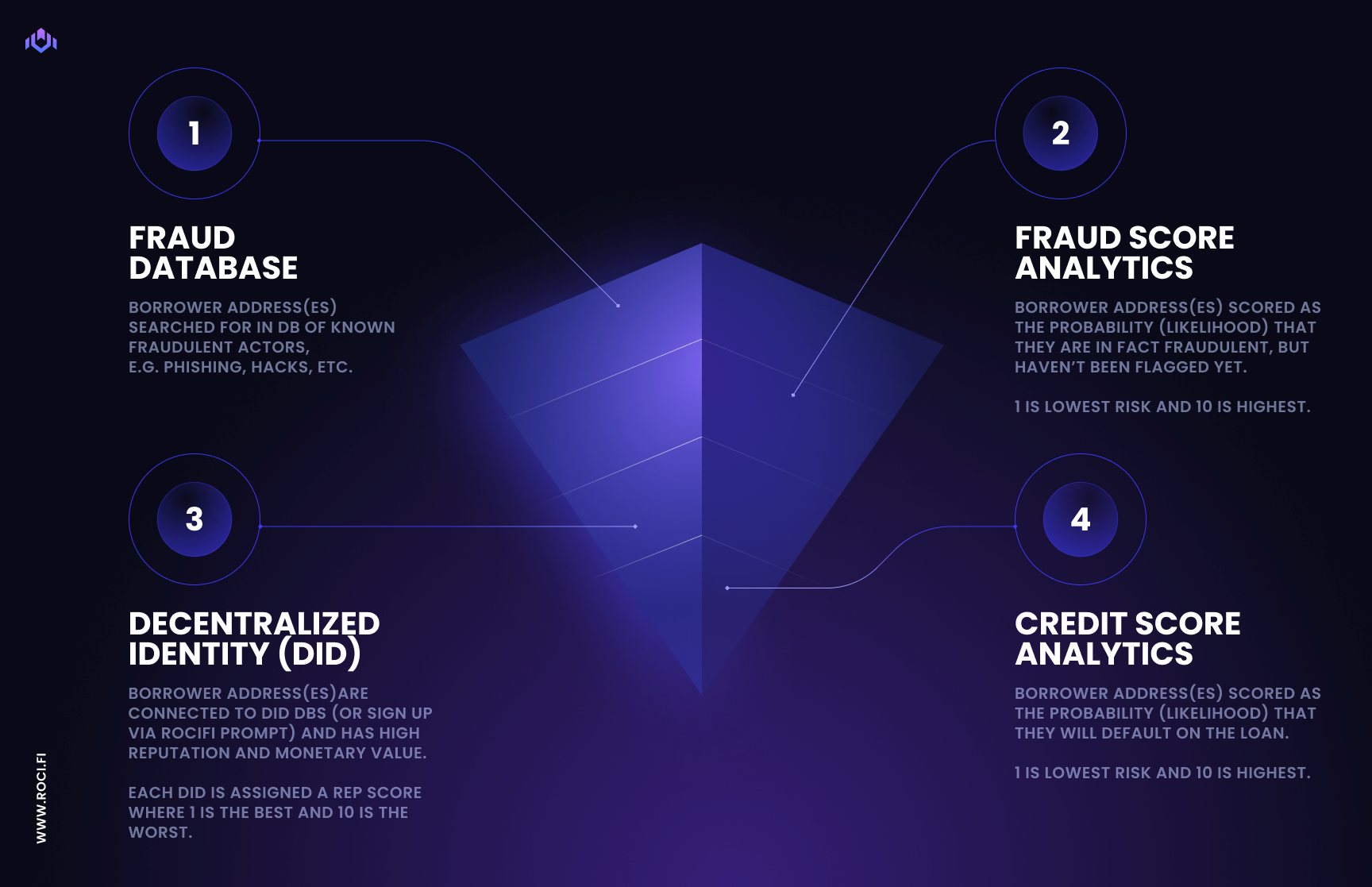

- RociFi introduces Non-Fungible Credit Scores (NFCS), allowing borrowers with clean on-chain histories to obtain loans with reduced collateral requirements, fostering capital efficiency and trust in DeFi.

A variety of innovative projects are pushing boundaries in this space:

- Spectral: Utilizes its Multi-Asset Credit Risk Oracle (MACRO) to analyze blockchain activity and mint Creditworthiness NFTs (cwNFTs), which users can leverage for preferential borrowing rates across the ecosystem. Read more at Chaindigi.

- CreDA: Offers decentralized ratings across multiple chains. Users mint their Crypto Credit Scores as cNFTs, unlocking access to leveraged and low-collateral loans via partnerships like FilDA (GlobeNewswire).

- Reputation DAO: Bridges DeFi with traditional finance data flows, using both real-world identity verification and on-chain analytics for robust risk management.

- RociFi: Introduces Non-Fungible Credit Scores (NFCS), enabling borrowers with clean histories to access under-collateralized loans, fostering greater capital efficiency.

The Mechanics of Blockchain-Based Credit Assessment

The core innovation behind decentralized credit bureaus lies in their ability to synthesize vast amounts of permissionless blockchain data into actionable insights. Unlike opaque traditional bureaus, these systems operate with full transparency while preserving privacy through cryptographic techniques like zero-knowledge proofs.

A typical on-chain credit score might incorporate:

- Lending and borrowing history across protocols

- Wallet age and activity frequency

- Diversity of protocol usage (e. g. , DEXs, yield farms)

- Liquidation events or default records

- Total value transacted over time

This granular behavioral analysis enables protocols like Credora and Spectral to offer dynamic risk models that adapt as users interact with the ecosystem. As highlighted by recent research from GARP and arXiv, building efficient on-chain credit scores represents a step-change innovation for uncollateralized lending markets, unlocking trillions in potential value as capital allocation becomes more precise.

The Road Ahead: Capital Efficiency and Fair Access

The impact is already tangible: lenders can allocate funds more confidently while borrowers gain fairer access based on merit rather than arbitrary requirements. Projects like zkCredit argue that these advances will bring trillions of dollars into DeFi by lowering barriers for both sides of the market.

However, the transformation is not just about unlocking capital - it is fundamentally reshaping the risk landscape of decentralized finance. With on-chain credit scores, protocols can calibrate interest rates, loan-to-value ratios, and liquidation thresholds in real time based on evolving user profiles. This dynamic risk pricing stands in stark contrast to the static, one-size-fits-all models that previously dominated DeFi lending.

For example, a borrower with a robust history across multiple protocols and no default events might receive lower collateral requirements and preferential rates. Conversely, wallets exhibiting erratic behavior or frequent liquidations will face stricter terms. This data-driven approach aligns incentives for both parties and fosters a more resilient lending ecosystem.

Privacy and Security: Decentralized by Design

One of the most significant technical advantages of decentralized credit bureaus is their commitment to privacy-preserving computation. By leveraging zero-knowledge proofs and advanced cryptography, platforms like Spectral and CreDA allow users to prove their creditworthiness without exposing sensitive transaction details. This ensures compliance with privacy norms while maintaining transparency for counterparties.

Moreover, because all data used in these assessments is sourced from public blockchains, the risk of data manipulation or centralized censorship is dramatically reduced. Users maintain control over their identities and financial histories through self-sovereign wallets and tokenized credentials like cwNFTs or cNFTs.

Key Benefits of On-Chain Credit Scores in DeFi Lending

- Reduced Collateral Requirements: On-chain credit scoring enables undercollateralized or even no-collateral loans by accurately evaluating a user's on-chain behavior and creditworthiness, improving capital efficiency for both lenders and borrowers.

- Personalized Loan Terms: Lenders can offer tailored interest rates and loan conditions based on individual on-chain credit profiles, resulting in a more competitive and user-centric lending environment.

- Enhanced Transparency and Trust: On-chain credit assessments provide verifiable, transparent, and tamper-resistant credit metrics, fostering greater trust between borrowers and lenders within decentralized protocols.

- Broader Access to Credit: By leveraging blockchain data, on-chain credit scores open lending opportunities to users who may lack traditional credit histories, promoting financial inclusion across global markets.

- Improved Risk Assessment for Lenders: Platforms such as Credora, Spectral, and CreDA empower lenders with real-time, data-driven risk evaluation, enabling more informed capital allocation and reducing default rates.

- Interoperability Across Platforms: Tokenized credit scores (e.g., cwNFTs from Spectral, cNFTs from CreDA) can be used across multiple DeFi protocols, allowing users to unlock better borrowing terms throughout the ecosystem.

Bridging Traditional Finance and Web3

The integration of on-chain credit scoring mechanisms also paves the way for greater interoperability between traditional financial systems and DeFi protocols. Reputation DAO’s model exemplifies this trend by analyzing real-world identity alongside on-chain activity - a step toward unified risk management frameworks that can span both domains. As more institutions explore blockchain-based lending, we can expect further convergence between conventional credit analytics and decentralized methodologies.

Ultimately, these advances do not just benefit crypto-native users; they extend financial inclusion to global populations previously excluded by legacy systems. On-chain credit scoring provides an open gateway to fairer borrowing terms, greater capital mobility, and trust-minimized lending markets.

What Comes Next?

The next phase for decentralized finance will be defined by continued innovation in blockchain credit assessment tools. As protocols refine their algorithms using AI-powered analytics and multi-chain data aggregation, expect even greater precision in risk modeling - benefiting everyone from individual users to institutional allocators.

The path forward is clear: as on-chain credit scores become ubiquitous across lending platforms, DeFi will evolve into a more efficient, equitable system where trust is algorithmic but opportunity remains human-centric.

No comments yet. Be the first to share your thoughts!